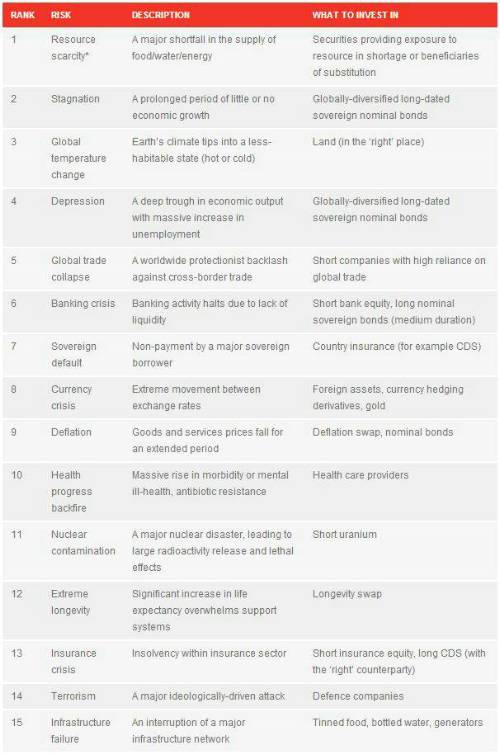

Towers Watson’s extreme risks ranking has a new top three: Food/water/energy crisis, Stagnation and Global temperature change – while Sovereign default and Insurance crisis have both fallen five places and Depression loses the top spot for the first time since the research began in 2009. While Food/water/energy crisis (previously Resource scarcity) rose ten places to take the top slot, other extreme risks that have also risen up the ranking this year are Global trade collapse (+4) and Global temperature change (+3). Extreme risks that, in Towers Watson’s view, are less of a threat than in 2011 include Sovereign default, which has fallen five places, as has an Insurance crisis, while a Currency crisis and a Banking crisisfell three and two places respectively.

Towers Watson’s research and ranking1, entitled Extreme risks 2013, categorises very rare events that would have a high impact on global economic growth and asset returns if they occurred. The top 15 Extreme risks now for the first time include: Stagnation, Health progress backfire, Nuclear contamination, Extreme longevity and Terrorism, while those that have dropped out of the top 15 this year are: Euro break-up, Hyperinflation, Political crisis, Major war, End of fiat money and Killer pandemic.

Tim Hodgson, head of Towers Watson's Thinking Ahead Group, said: “There has been a high level of turnover in the top 15 this year. This is largely due to us expanding our research into the non-financial extreme risks so that we now have a full list of 30. So while on the face of it, it’s good to see the likes of Killer pandemic and Major war dropping out of the top 15, they are only just below the cut off (at 17 and 18 respectively). New entrants to the top 15 include the likes of Terrorism and Extreme longevity which rise up the rankings either due to our assessment that they are more likely (Major terrorist attack rather than World war III) or there is less uncertainty as to the impact (Extreme longevity vs. Killer pandemic). This illustrates the challenge facing institutional investors, of how they should actually adapt to changing assessments of extreme risks. We would suggest that time should be spent on ‘pre mortems’ which are about trying to determine in advance what could, colloquially, ‘kill you’, that is permanently impair an investor’s mission.”

According to the research such ‘pre mortems’ should identify which extreme risks matter and which can be ignored. For the former, Towers Watson asserts that the right thing to do is to pay up for the insurance (if available and affordable), given that the prioritisation exercise has shown the investor cannot afford to self-insure. Then an investor should do the simple things: ensure the portfolio is as diversified across as many return drivers as possible; diversify within asset classes; and create a strategic allocation to cash to provide optionality. Thereafter, it suggests that greater complexity can be added over time, assuming these steps pass a considered cost/benefit analysis, such as adding long-dated derivative contracts in a contrarian manner, that is, when they are cheap rather than popular.

Tim Hodgson said: “While interesting in its own right, we believe the consideration of extreme risks can be useful in helping to design more robust investment portfolios and more robust risk management processes. The starting point to building a robust investment portfolio and reducing (but not eliminating) tail risks is to introduce greater diversity. The next step is to explore some hedging strategies.”

The Towers Watson research suggests, broadly, there are three hedging strategies available to institutions:

-

Hold cash. The option value of holding cash increases in periods of market stress, allowing investors with cash to buy truly cheap assets.

-

Derivatives. It is worth mentioning that cost and usefulness are often in opposition. The cost of derivatives protection can often be reduced by specifying more precise conditions – but the more precise the conditions, the greater the chance that they are not exactly met and hence the ‘insurance’ does not pay out.

-

Hold a negatively-correlated asset. There is no single asset that will work against all possible bad outcomes. Further, there is no guarantee that the expected performance of the hedge asset will actually transpire in the future event.

Tim Hodgson said: “We believe that being adept at ‘pre mortems’ means being a better risk manager, and being able to react more flexibly in the event of an extreme event happening, particularly as the event is unlikely to evolve precisely as predicted. Consequently, the obvious application of extreme risk thinking is in stress-testing or scenario planning, but it is also constructive to consider whether the thinking can be incorporated within the process for managing an investment institution’s balance sheet.

“Naturally, we would advocate establishing some sort of early warning system to closely monitor what could develop into extreme events. While this is probably one of the areas where things are easier said than done, the science (and art) of predicting the seemingly unpredictable has advanced significantly during the global financial crisis.”

1 A subjective scoring system to derive a ranking of these risks, and the change of ranking reflects a change of view regarding both impact and likelihood of each individual risk.

* Food/Water/Energy crisis

* Food/Water/Energy crisis

** Our subjective measure based on the intensity and scope of the impact, the likelihood, and the degree of uncertainty in assessing the risk level.

|