Hymans Robertson modelling shows that the new Pensions UK Retirement Living Standards (RLS) ‘comfortable’ retirement level remains out of reach for most pension savers once housing costs are factored in. The recent Retirement Living Standards (RLS) are based on expenditures in retirement that do not include ongoing housing costs for retirees. When factoring in housing costs, the leading pensions and financial services consultancies Guided Outcomes(GO)TM modelling shows that the likelihood of meeting retirement goals falls sharply, particularly for lower and middle earners. This firm warns that, for many savers, a comfortable retirement will increasingly depend on working for longer, contributing more throughout their career, or a combination of both. It says that Trustees, providers and employers must support members to set realistic retirement goals and regularly review whether they remain on course to meet them.

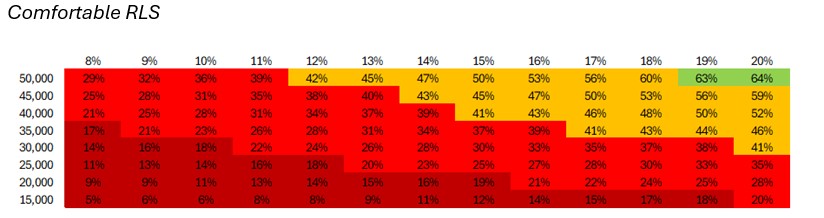

In its updated modelling, the firm found that someone earning £50,000 a year and contributing at the current auto-enrolment minimum level is unlikely to have a good chance of achieving a ‘moderate’ retirement living standard. A saver earning £30,000 would need to contribute around 17% of salary throughout their working life to have better than a 50% chance of reaching that standard. Meanwhile, a ‘comfortable’ retirement remains out of reach for many, with someone on average earnings needing to contribute more than 20% of salary to have a good chance of achieving it.

Commenting on the updated modelling, Kathryn Fleming, Head of DC Consulting, Hymans Robertson, said: "The updated RLS provides a helpful benchmark for understanding the kind of lifestyle pension savers may be able to achieve in retirement. While everyone's circumstances are different, our modelling shows that many people will struggle to reach the higher standards without making significantly larger pension contributions than are currently required under auto-enrolment.

"Trustees, employers and providers all have an important role to play. Whether that's ensuring contributions are invested effectively, designing workplace benefits that encourage better saving habits, or providing tools and support that help members understand their options, helping people achieve better retirement outcomes requires action across the pensions industry."

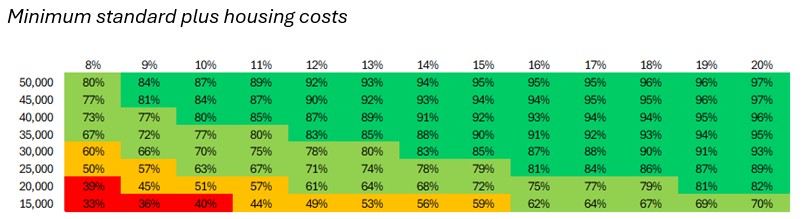

Housing costs are an increasing challenge for savers. When rental costs are added to the minimum RLS, even a saver on close to average earnings contributing more than the auto-enrolment minimum could still face a one-in-four chance of falling short of that standard. Lower earners would need to contribute significantly more than the current minimum contribution level to achieve the same outcome.

Commenting on the housing cost impact to retirement savings, Hannah English, Head of DC Corporate Consulting, Hymans Robertson, said: "Housing is one of the biggest challenges facing younger generations. The Retirement Living Standards assume housing costs have been removed by retirement, but that will not reflect the reality for everyone. Many savers face difficult decisions between putting money aside for a home deposit and saving for retirement, and the long-term consequences of delaying pension saving can be substantial.

"With increasing focus on retirement adequacy, including work currently underway across the industry, and with pensions dashboards set to bring retirement savings into sharper focus. More people may become aware of the gap between their current savings and the retirement lifestyle they hope to achieve. At this point its highly likely that employees will turn to their current employers to understand how to ‘fix’ this. The Pensions Commission will be important to reviewing AE minimum rates, but employers have a role to play in considering the needs of their unique workforces and the ‘right’ levels for them.”

|