|

|

Inconsistent regulation is creating barriers to widespread and rapid carbon capture, transport and storage adoption, but insurance could help to fill critical gaps. Carbon capture, transport and storage (CCS) is one of the few scalable pathways for natural resources companies to reduce emissions, meet regulatory requirements, create new revenue streams, and protect long-term asset value while enabling businesses to continue to use their assets profitably as they decarbonize operations. |

By Marie Reiter, Head of Global Broking Strategy Natural Resources, WTW However, complex risks exist along the value chain, which affect the bankability of CCS projects, and have slowed investment in the technology. Insurance could play a critical role in bringing more CCS projects to market. Insurance products that work across the value chain and fill current coverage gaps can make investments in the technology more viable, as they open up financing options for developers. Natural resources companies looking to develop CCS projects must understand the regulatory landscape as it stands and how the right insurance strategy can help them unlock protection for their carbon credits. The critical issue: A patchwork of regulation

Investment in CCS depends on robust regulatory frameworks. Regulation determines when businesses can obtain carbon credits, which party is responsible for CO2 at different parts of the value chain, and for how long storage must be managed. Ultimately, these regulatory frameworks determine whether a CCS project is commercially viable.

“There is a clear correlation globally between territories that have implemented clear CCS policies and pace of CCS development in these areas. The market demand for CCS is only there when legislation and regulatory policies are implemented by government. If the cost of CCS exceeds the tax savings/carbon credit value, or if the carbon credits are lost due to leakage or loss, then the project value proposition no longer stands up,” says Marie Reiter, Global Head of Broking Strategy, Willis Natural Resources. No standard regulatory framework for CCS exists – instead, there is a patchwork of regulation across different geographies, which can directly impact the viability of a CCS project. But inconsistent or incomplete regulation across capture, transport, storage, and cross border movement directly amplifies the financial, operational, legal, and strategic risks that natural resources companies face when deciding whether to develop CCS projects. These elevated risks translate into slower adoption, deferred investment decisions, and difficulty securing financing. Risks associated with CCS projects:

Financial: Uncertain revenue models are harder to finance, leading to a higher cost of capital or the need to fund developments from equity

Regulatory/compliance: Unclear future requirements (e.g., monitoring obligations) can increase the risk of stranded assets – carbon market volatility or policy change can make assets redundant

Operational: Lack of harmonized safety, purity and transport standards create project integration challenges

Strategic: Companies avoid committing to CCS investments until regulatory frameworks stabilize

Slower ecosystem development: Infrastructure such as pipelines and storage networks cannot scale efficiently without regulatory alignment, slowing overall adoption

CCS regulation can behave as ‘carrots’ or ‘sticks’:

Carrots: Government subsidies, carbon credits, grants and funding are some of the incentives for making decarbonisation financially attractive. They can boost early adoption of clean technologies, in turn making CCS and carbon markets more politically palatable and economically feasible. Carbon credit markets are expanding, but they do not exist in every country. Without these incentives, the economics would not work.

Sticks: Carbon taxes, mandatory emissions reductions and penalties for non-compliance are among the disincentives for emitting carbon. Research shows that such ‘sticks’ are necessary, as incentives alone cannot achieve the significant reductions in emissions required.

There is no one-size-fits-all approach to CCS regulation. As government involvement in CCS projects varies from country to country, so too do their regulatory frameworks. Jurisdictions with minimal government control, including Norway and the Netherlands, tend to rely on a combination of ‘carrots’ and ‘sticks’ to drive investment in the technology. Clear and appropriate regulations not only reduce risk for natural resources companies, making CCS deployment financially viable, they are also strategically aligned with national decarbonization goals. A deeper dive: The CCS regulatory maturity scale

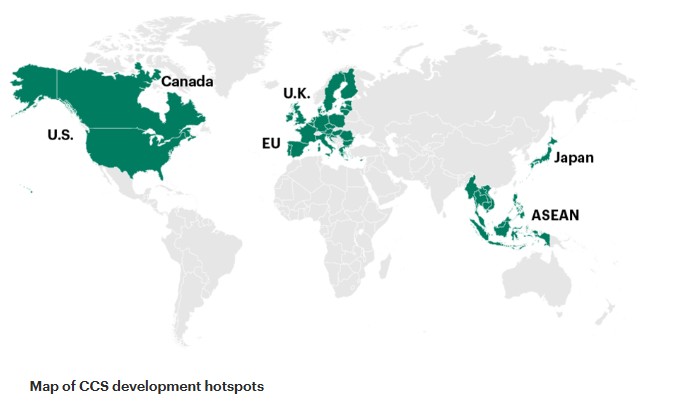

Jurisdictions’ regulatory frameworks also vary in terms of their maturity. While some geographies, including Japan and the European Union, have more advanced regulatory frameworks (Japan’s CCS Business Act is aimed at attracting private sector investment), others, such as Malaysia and Indonesia, are catching up fast. Over 2023 and 2024, Indonesia introduced four major CCS regulations, establishing one of the region’s most detailed schemes.

CCS development hotspots Japan:

Key regulations:

Japan’s landmark “Act on Carbon Dioxide Storage Business” (CCS Business Act), effective August 2024

The value:

The most complete regulatory framework in Asia

Strong funding

Cross border legal clarity, and national coordination

Clear pathways for project to move forward

The European Union

Key regulations:

International treaty: London Protocol (1996 + 2009 amendment)

CCS Directive (Directive 2009/31/EC)

Industrial Emissions Directive (IED) (Directive 2010/75/EU)

EU ETS Directive (Directive 2023/959/EU)

Renewable Energy Directive (RED II/III) (Directive 2018/2001/EU)

Removals & Carbon Farming Regulation (Reg. 2024/3012/EU)

Net-Zero Industry Act (Reg. 2024/1735/EU)

TEN E Regulation (Reg. 2022/869/EU)

The value:

Comprehensive regional regulation

Industrial strategy integration

Infrastructure coordination

Standardization of approach across multiple countries and jurisdictions

United Kingdom

Key regulations:

International treaty: London Protocol (1996 + 2009 amendment)

The Energy Act 2023

The value:

Robust regulation across transportation and storage

Actively addressing gaps (like non pipeline transport) and building market driven networks

Meaningful government support package for all value chain participants

Government acts as insurer of last resort

United States

Key regulations:

Federal tax incentives – Inflation Reduction Act Section 45Q tax credit

EPA Underground Injection Control (UIC) Program – Class VI Wells

Federal policy framework such as Carbon Capture Coalition’s Federal Policy Blueprint and Carbon Removal RD&D Priorities (FY2026)

Evolving EPA reporting requirements

The value:

Significant financial incentives reduce project costs and accelerate deployment

Flexible verification pathways (e.g., IRS Notice 2026-01 safe harbor) lower compliance risk and help projects maintain credit eligibility

Strategic roadmaps provide a clear, coordinated policy environment that de-risks scale-up

Canada

Key regulations:

Federal CCS Investment Tax Credit (ITC)

Provincial carbon pricing & incentives such as Alberta’s TIER - Carbon Sequestration Tenure Regulation, Alta Reg 68/2011 (Alberta), Carbon Capture and Storage Funding Act, SA 2009 cC-2.5 (Alberta, 2009, Carbon Capture and Storage Statutes Amendment Act, 2010, SA 2010, c 14 (Alberta), EOR Quantification Protocol (Alberta)

Regulatory frameworks for pore space, liability, and MMV. Federal and provincial funding programs such as Federal and provincial funding program including SIF, Carbon Capture Kickstart, ACCIP (12% capital incentive), and Saskatchewan Technology Fund

The value:

High-value capital incentives significantly lower upfront investment barriers

Provincial pricing systems create strong CCS revenue pathways

Federal and provincial funding programsprovide layered support across feasibility, FEED, and capital build phases

These regulatory frameworks reduce risk for natural resources companies and make CCS deployment financially viable, scalable, and strategically aligned with national decarbonization goals.

How insurance can help protect complex disintegrated CCS value chains

Although several parts of the CCS value chain fall within the scope of traditional insurance markets, coverage gaps remain. The insurance industry is working to fill these gaps to build more resilient protection for the CCS value chain.

No two CCS projects are alike, and no best practice yet exists for unlocking the value from carbon capture projects. The network of risks and complexities increase exponentially when spanning multiple jurisdictions and territories. Differing legal regimes, liability frameworks, carbon accounting rules, and permitting requirements can create misalignments between parties and introduce liability gaps. By assessing risks across the entire value chain in its entirety, parties can better map their liabilities and contractual obligations, and ensure suitable insurances are in place.

Natural resources companies should choose modular insurance solutions that are tailored to each project, and that have the flexibility to adapt to exposures across different regulatory regimes.

CCS projects inherently contain significant interdependency risk, with any issue at one point in the chain causing delays and financial loss for the remaining parties. For example, a leakage occurring at the storage site could halt the injection of any additional CO2. The transport operator may then be unable to load or unload, preventing the emitter from capturing additional CO2 once their on-site storage becomes full, which could ultimately lead to curtailment of the asset.

The viability of CCS projects depends on each part of the value chain aligning with the rest. Failures in any one link, whether that be through operational disruption, misaligned liabilities, or non-compliance with regulations, could cause the entire chain to unravel.

Due to the interdependencies throughout the value chain, those developing CCS projects will need to collaborate with counterparties and their insurance providers to construct a solution that protects the entirety of the value chain, rather than considering individual siloed risks. This way developers can strategically align liabilities and insurance solutions.

To make insurance as effective as possible, natural resources companies must involve specialist brokers early, allowing them to input into contract negotiations and allocate liability to optimize insurance protections and unlock bankability.

|

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd