|

|

The Actuarial Function Report (AFR) is key for meeting regulatory standards and reassuring Boards and stakeholders. However, the time spent on these reports can limit actuaries' ability to offer practical business insights. In this paper, we discuss practical ideas for transforming the AFR into a tool that not only meets regulatory expectations but also enhances the Board’s understanding of business risks, performance and opportunities. |

By Matthew Pearlman. Partner and Daniel Sacks, Analyst, LCP We focus on putting into practice three key principles that should underpin every stage of the Actuarial Function’s (AF) opinion:

Target value-add, not (just) compliance We provide practical tips and steps in each section to help the AF add more value, engage in decision-making promptly and continuously improve processes in line with best practices.

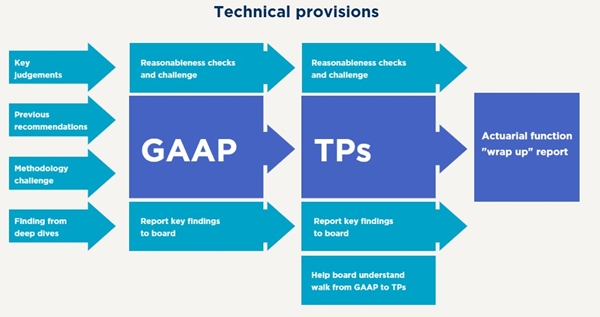

Technical provisions We see the TP exercise as an ongoing process, not just a final report, where valuable insights will emerge throughout. The AFR records these insights even if it is not the main way they are initially communicated. An ideal project plan could be structured as follows:

Typically, TPs build on the foundation of GAAP reserving. Planning should start before starting the GAAP reserving process, with a focus on making recommendations that can add value. These recommendations should be reviewed and carried forward into the following year, ensuring they are implemented effectively. This approach supports an iterative reserving process, driving meaningful improvements year after year. This could involve, for example, improving data flows across the system or properly implementing the reinsurance programme into the calculations. Additionally, it is worth revisiting the key judgments made and the methodological challenges recorded in the previous year. These elements should be incorporated into the planning phase before the annual reserving process begins. We find the quiet period before the annual year-end reserving process an ideal time to conduct deep dives. For example, this time could be used to assess case reserving adequacy, using the broader perspective offered by the reserving exercise on the claims process. Insights from these deep dives can then be incorporated into GAAP reserving and subsequently into the TPs, ensuring they do not become an additional strain on resources during the critical first-cut reserving phase. We suggest that the TP report focus on two key parts: Value-add: Explaining the walk from GAAP reserves to Solvency II reserves, which is typically shown as a waterfall chart. In our experience, this is poorly understood by all but those close to the analysis. The Board needs to understand the sensitivities around individual items in the waterfall and when they could be potentially material Compliance: Picking up the important points from GAAP reserving and ensuring that they are all documented within the TP report. Most reserving insights should ideally be highlighted earlier in the process.

The underwriting opinion Some of the most effective challenges raised by actuaries are simple yet impactful. For example, questioning assumptions such as “What is our justification for assuming we can increase business volumes while also increasing premium rates?” can prove insightful. Similarly, comparing business plan loss ratios to historical trends can highlight potential issues, such as unrealistic expectations that historical loss ratio deterioration will reverse through “re-underwriting” efforts alone. It is important to present facts in a way that the Board can easily understand. For example, showing how much advance credit is being assumed for underwriting changes can help the Board assess whether such assumptions are reasonable. We suggest framing facts in terms of their impact on decisions, to ensure that the Board has the information needed to make right choices.

Best Practice

AF clearly involved while business plan is still live, challenging assumptions appropriately.

Initial AF recommendations given before board signs off business plan

Good Practice

Balanced framework for giving credit to 're-underwriting' arguments

Appropriate challenge of potentially heroic assumptions

Behaviours to avoid

AF under pressure to justify reasonableness of business plan in arrears

AF conclusions not sufficiently objective or rooted in analysis of historical data

The Board should receive the actuary’s initial observations and challenges before approving the business plan, even if they are not yet formalised into an official opinion. Early engagement can help to ensure that the actuarial perspective is integrated into the planning process and adds meaningful value.

Reinsurance opinion The reinsurance opinion usually comes after the main reinsurance purchase decisions, offering a chance to independently assess the quality of MI and look at the decision from a different angle. A common issue identified in these opinions is the imbalance between qualitative and quantitative information provided to the Board, with the latter often lacking the detail needed for fully informed decisions. Below are some ideas to enhance the value of the reinsurance opinion for the business.

Using the right metrics For example, the reinsurance policy may state that no single reinsurer should have more than 20% of any layer. While it is normally clear whether this technical limit has been breached, reviewing the entire programme can reveal surprising levels of reliance on one reinsurer. This may then highlight that the policy has not been expressed clearly, providing the opportunity to clarify the risk appetite and improve future reinsurance decisions. Another effective approach is to supplement actuarial modelling results with tests against historical experience. Board members will likely remember the company’s worst recent year and will want to see how the reinsurance programme would have responded to those losses. We often find that clearly explaining any differences, such as changes in line sizes or improved terms and exclusions, can help the Board in understanding how those past losses relate to today’s exposures.

Best practice

Clear understanding of how emerging risks are built into either pricing or policy exclusions.

Clear articulation of firm's appetite to accept certain emerging risk in new business.

Good practice

Clear link between the emerging risk framework and actuarial processes.

Consideration of external factors which may limit the ability to deliver the business plan.

Behaviours to avoid

Little consideration of emerging risks or their materiality.

Little involvement to the AF in emerging risks discussions. Poorly defined emerging risks framework.

It is important to state the obvious. For example, “This programme leaves us exposed to a third post $10m loss, but the modelled probability of such a scenario is very low and in the history of the company there has only ever been one loss over $7m in a single year”. What seems obvious to one person may not be clear to someone else or may be overlooked amidst the many other factors being considered.

Governance of information is another key area for the reinsurance opinion. For example, if reinsurance modelling relies on a capital model calibrated to a 1-in-200 level for capital setting, it may be less reliable at the 1-in-10 or 1-in-20 levels typically used for reinsurance decisions. It is important for the opinion to communicate these limitations, helping the Board to understand implications of relying on such data.

Feedback loops

Contribution to risk management

Risk appetite

The AF’s involvement should start early in the development of the risk appetite statement, rather than reviewing it once finalised. This ensures alignment with the company’s strategic objectives and the inclusion of clear, quantifiable measures to enhance clarity and usability.

Objective metrics in the risk appetite framework can help the AF to assess business plans and are highly valued by the Board. A clearer, more measurable risk appetite statement enables the Board to engage more effectively with the company’s overall risk strategy.

Own Risk and Solvency Assessment (ORSA)

The AF should play a fundamental role throughout the ORSA process. While ownership of the ORSA often sits with the risk management team, the AF should be actively involved at every stage, from planning to finalisation

In some jurisdictions, such as Ireland, the head of the Actuarial Function is required to provide a formal report on the ORSA, covering areas such as:

The range and robustness of stress and scenario testing.

Limitations of the scenarios and their potential impact. The alignment of ORSA results with the company’s capital requirements.

This highlights the value of the AF’s input in the ORSA process, even if formal reporting is not required. By contributing to its development and review, the AF can ensure that the ORSA is robust, well-aligned with risk appetite and connected to the company’s capital planning processes.

Risk committees

The AF is a key participant in risk committee discussions and should actively contribute to these meetings. We suggest having regular one-to-one interactions with Board members, the chair of the risk committee and other committee members, to help build strong relationships and ensure alignment on key risk issues. Regular input from the AF can help to ensure that actuarial insights are considered when making strategic decisions.

Other general considerations

Timing of the report For example, the Underwriting Opinion, or at least the initial findings, should be presented to the Board while the business plan is still live and where any key challenges from the Actuarial Function can still be factored into the plan by the Board. Another example is the AF’s involvement in the Own Risk and Solvency Assessment (ORSA). Before the Board signs off the ORSA, they should have the benefit of input and challenge from the AF.

Structure of the report We suggest some simple changes below that can make a big difference to how the audience engages with the findings of the report:

Putting the opinions and key recommendations on page 1. This helps Boards focus on the purpose of the report. |

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd