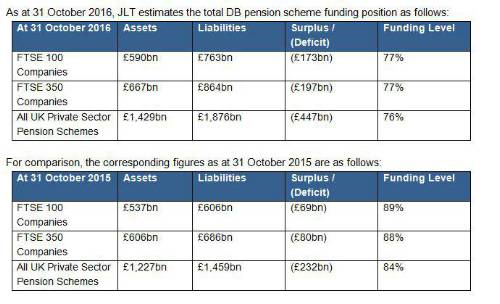

Charles Cowling, Director, JLT Employee Benefits, comments: “This last month has seen an easing in deficits from the record heights of over £500 billion recorded at the end of August. But deficits have still doubled over the last 12 months and there appears no relief in sight for companies with large pension schemes. Some have argued that in light of unprecedented market conditions, there should be a review of how pension deficits are calculated. But this misses the key point that the size of the problem we face today is the inevitable consequence of a regulatory system that is looking to guarantee that members’ benefits are paid. If we want those guarantees, and it would take a brave politician to seek to remove them or water them down, then we have to accept that they are very expensive. Simply changing the method of measurement solves nothing.

“So what can trustees and companies do? Well, difficult problems require creative solutions. There are no easy answers, but pension schemes can make life easier by following a three point plan:

1. Taking every opportunity in volatile markets to reduce risk at an acceptable price. This may mean close, possibly even daily, monitoring of pension scheme assets and liabilities and, using triggers, looking for opportunities to take advantage of favourable pricing.

2. Looking at all options to reshape liabilities and settle liabilities through member exercises, such as the payment of transfer values that can ease the burden of pension schemes deficits and give members valuable options.

3. Implement an integrated risk management framework that takes advantage of alternative ways of providing security to pension scheme members. For example, where there is a strong employer then it is reasonable that the employer be allowed to take more risk, and get more relief, in the funding and investment strategy, through a longer recovery period. Similarly if it is possible for the employer to provide alternative security to pension scheme members this may allow some relief from the otherwise inevitable demands for significant hikes in funding contributions.

“Companies and trustees should leave no stone unturned in their search for less costly ways of ensuring that members get their promised benefits without massively disadvantaging shareholders.”

|