By Matthew Paton, Actuary at Barnett Waddingham

One consequence of the higher-yield environment is that, all else being equal, exit payments calculated on a “minimum risk” basis, which in the Local Government Pension Scheme (LGPS) are typically calculated using gilt yields, are now lower. Good news, perhaps, for employers with one eye on leaving the LGPS and who are now closer to being able to afford the exit payment.

However, typically, these employers will not have a formal guarantor in their fund ready to take on the pension liabilities for the remaining members when they leave. Therefore, funds want to be prudent to ensure they have sufficient monies to pay future benefits and protect other participating employers from having to meet these costs.

Background

The idea behind calculating an exit payment based on gilt yields is that it broadly replicates what happens in the private sector, when a pension scheme wishes to “buy out” its liabilities and pass them on to an insurer. That insurer will typically look to the gilt market to calculate the premium for accepting these liabilities (with some loading for profit and expenses), the theory being that they can use the premium to purchase gilts and receive a near guaranteed return from the Government.

There is no current provision for LGPS benefits to be bought out in this way, although the gilts-based approach has been a common proxy for calculating exit payments for many years. In this case, the role of “insurer” is taken on by the remaining employers in the fund, who are essentially on the hook for additional contributions in the scenario of adverse future funding experience. Using this approach, exit payments tend to be relatively high and so have had the effect of protecting funds, as it reduces the risk of calling upon their remaining employers to meet any future deficit that could arise.

Unlike an insurer, most LGPS funds will not use the exit payment just to purchase gilts, but will instead invest it in line with the fund’s Investment Strategy Statement. The term “minimum risk” is therefore something of a misnomer, as investment risk is often left on the table. There are of course other risks which remain though, such as longevity and inflation risk.

The impact of rising yields

As gilt yields have crept up, exit payments have been falling. But can the same really be said for the risks that funds are facing? Many of these risks have been around for a number of years now, such as the ongoing effects of Brexit and the Covid pandemic. At this round of England and Wales valuations, we also have war in Ukraine, double digit inflation and the looming prospect of a lengthy recession. It does not at first glance seem that the level of risk is any lower than it was three years ago, although on the current methodology that most LGPS funds have in place they will be charging significantly less in the way of exit payments.

It was not too long ago where most of the talk regarding exit payments was in relation to their unaffordability for employers wishing to leave. The introduction of Deferred Debt and Debt Spreading Arrangements provided flexibilities to manage exit payments in such circumstances.

At the time of writing, much of the volatility in gilt yields seen in the autumn has subsided but yields have since resumed a slow ascent. Future volatility also remains possible and interventions from the Bank of England such as quantitative easing or tightening may mean that the gilt market will at times be distorted, unduly affecting minimum risk valuations.

Source: Bank of England UK nominal spot curve

At their peak, gilt yields reached 5.2%, which is higher than the ongoing discount rate of some LGPS funds. Left unreviewed, this could lead to a somewhat absurd scenario of lower exit payments being requested from employers who have no guarantor in their fund compared with those that do.

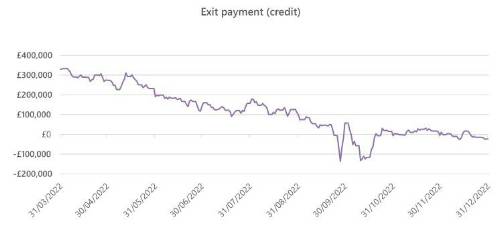

Case study

Below we illustrate how the exit payment may have progressed since 31 March 2022 for an example employer destined to exit under the minimum risk basis. We have also assumed an investment strategy of a typical LGPS fund.

The results in the chart show how volatile the possible exit payment has been using the minimum risk basis over a relatively short period of time. Note that a negative value of the exit payment indicates an exit credit may be due, subject to the details of the Funding Strategy Statement.

What does all this mean for LGPS funds?

In terms of ongoing funding levels and required contributions, the impact on employers is expected to be limited.

However, when it comes to minimum risk exit valuations, the outcomes illustrated in our case study above may not be considered entirely desirable by funds or employers. Ultimately, the aim of an exit policy should be to ensure the fund remains suitably protected, while considering fairness and affordability to exiting employers. It is important to ensure this balance remains appropriate.

|