Analysis of the latest ONS data on the private sector defined contribution (DC) market from leading independent consultancy Broadstone uncovers a surge in lump sum access around both the 2024 and 2025 Autumn Budget.

Typically, savers can withdraw up to 25% of their pension pot tax-free, however there were rumours that the Government was considering restricting that allowance in both the Autumn Budget 2024 and 2025 as it looked to increase its tax revenues.

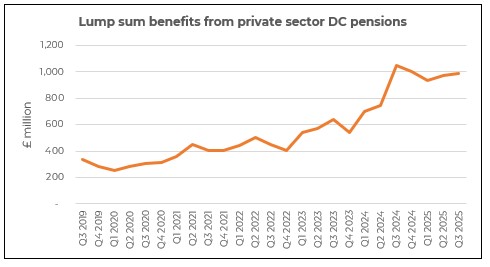

In the period Q4 2024-Q3 2025, savers took £3.9 billion of one-off cash payments from their pension pots. This marked an increase of 29%, or £868 million, compared to the previous 12 months in 2023/24 and an increase of 81%, or £1.7 billion, compared to the same period in 2022/23.

There are also clear spikes evident in both quarters near the Autumn Budget 2024 with lump sum access reaching record levels of £1.0bn in both Q3 2024 and Q4 2024 around the Chancellor’s statement on 30 October 2024.

Lump sum access then dropped back in the next two quarters before seeing another spike of £990 million in Q3 2025 before the Autumn Budget held on 26 November of that year.

The trend of increasing lump sum access is expected as more adults with DC pensions reach Normal Minimum Pension Age. However, the timing of recent spikes suggests that saver behaviour is being influenced by policy uncertainty and speculation around potential changes to the tax treatment of pension lump sums.

Kelly Parsons, Head of DC Proposition at Broadstone, commented: “This data highlights just how sensitive pension savers can be to speculation around tax and policy changes. It demonstrates the damaging and long-lasting negative impacts that rumour-mongering around pension policy and fiscal events can cause.

“Taking money from a pension is a complex and irreversible decision so it is critical that people aren’t making these important choices based on rumour or without full awareness of the consequences. That’s where better financial education and clearer guidance really do matter.

“As the DC market grows, employers will have a bigger role to play in supporting people as they navigate these decisions. That means clearer communication and making sure staff can access the right guidance and support, so they’re not just reacting to headlines but making choices that genuinely support their long-term retirement outcomes.”

|