Following last week’s Bank of England decision to hold interest rates at 3.75%, many homeowners may be breathing a sigh of relief. But after a year of stubborn inflation and global instability keeping borrowing costs higher for longer, those nearing the end of cheaper fixed-rate deals are still facing a sharp jump in monthly outgoings – with potential knock-on effects for long-term retirement savings.

New analysis from the retirement specialist Standard Life highlights the trade-off between managing higher costs today and protecting future financial security, showing how money absorbed by higher mortgage repayments could make a significant difference if directed into a pension instead.

With average five-year fixed mortgage rates rising from 4.91% at the start of the year to 5.63% as of June1, someone remortgaging onto a new £500,000 repayment mortgage over 25 years today would pay around £213 more each month than they would have done at the start of the year.

The impact could be significantly greater for borrowers coming to the end of older fixed-rate deals secured when interest rates were much lower. Someone moving from a mortgage rate of 2.50%, secured in 2021, to 5.63% on a £500,000 repayment mortgage over 25 years could see repayments rise by around £866 a month.

The potential retirement trade-off

While keeping up with mortgage repayments will naturally be the priority, higher monthly housing costs can reduce the amount available for other long-term savings, including pensions.

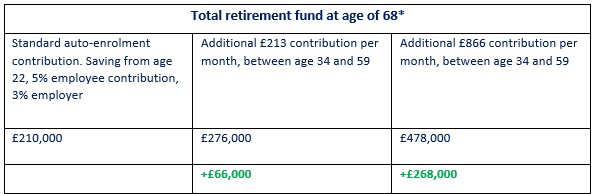

Standard Life analysis2 finds that someone who began working at age 22 with a salary of £25,000 and paid the minimum monthly auto-enrolment contributions throughout their career could build a total retirement fund of £210,000 by age 68.

If that person was able to contribute an additional £213 a month into their pension between the age of 34 (average age of a first-time buyer) for 25 years (average mortgage repayment period) their projected fund could rise to £276,000 - £66,000 more in today’s prices.

For someone able to contribute an additional £866 a month. the equivalent of the increased payments when moving from a 2.5% to a 5.63% mortgage rate, the pension benefit is greater, with the final retirement pot reaching £478,000 - £268,000 more than with minimum contributions alone.

*Assumptions: Starting salary £25,000, rising by 3.5% each year, 5% employee and 3% employer monthly contributions, 5% annual investment growth. Figures are reduced to take effect 2% inflation. Annual Management Charge of 0.75% assumed. The figures are an illustration and are not guaranteed. Earning limits not applied.

Mike Ambery, Retirement Savings Director at Standard Life, said: “The Bank of England’s decision to hold rates may provide some reassurance for borrowers, but with rates still expected to stay higher for longer, many homeowners refinancing this year are still facing a sharp jump in monthly repayments compared to the deals they’ve become used to.

“For those coming off lower fixed-rate mortgages taken out before the recent rise in interest rates, the increase in costs can be significant. That’s putting real pressure on household budgets at a time when many people are already contending with higher day-to-day expenses, and may lead them to reassess their wider finances.

“For many people, buying a home is a key part of their long-term financial security. But as mortgage costs rise, households may have less flexibility to save elsewhere, including into their pension.

“If someone needs to adjust their finances, reducing pension contributions may feel like a quick way to free up income. However, stopping altogether can make it harder to stay on track for retirement. Where possible, maintaining some level of saving can help protect your long-term retirement savings.”

Mike Ambery shares his tips on how to balance saving for your future with living now when costs are high:

Make your money work as hard as possible: “When budgets are tight, it’s important to get as much value as possible from what you can afford to save. Pensions benefit from tax relief, meaning the government effectively adds to your contributions - for example, £80 is typically topped up to £100 for basic-rate taxpayers. If you pay higher- or additional-rate tax, you can usually claim back more through your self-assessment tax return or by contacting HMRC, reducing the true cost further.

“How this works depends on your scheme. Some workplace pensions use salary sacrifice, where contributions are taken before tax, so you get the benefit straight away. In others, the top-up is added by your provider, and you may need to claim any extra relief yourself. Many employers also match your contributions, boosting your savings further - so it’s worth checking how your scheme works to avoid missing out. Over time, these combined boosts, alongside investment growth, can make a meaningful difference to your retirement pot. Investments can go down as well as up, but if retirement is some way off, staying invested gives your money longer to recover and grow.”

Stay consistent – even if you need to adjust: “If costs rise, it can be tempting to pause pension saving altogether. But that can mean missing out not just on tax relief, but on valuable employer contributions too - effectively turning down part of your pay. If you can, consider reducing contributions rather than stopping completely, so you maintain the habit and keep money flowing into your pension. Even small, regular payments can help avoid a much bigger catch-up later.

Track down old pension plans: “Finding old pensions can give you a clearer picture of your overall retirement savings and help you understand whether you’re on track. It’s worth using the government’s Pension Tracing Service if you’ve changed jobs, moved house or had more than one pension.

Review your wider outgoings: “Before cutting long-term savings, look across your regular spending to see whether there are areas where you can reduce costs. Setting a budget can help show where money is going and where there may be opportunities to shop around or cut back.

Know where to go for help: “If you’re struggling to keep up with costs, support is available. MoneyHelper has useful tools and guidance, and your pension provider may also have resources to help with debt, life events, health and other issues that can affect your ability to save.”

|