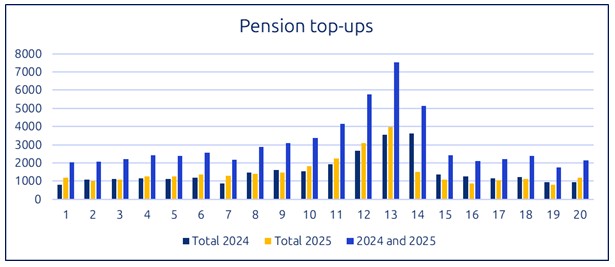

As people look to make the most of their finances at tax year end, Standard Life - a retirement specialist focused entirely on retirement savings and income - has identified this week, the 13th week of the year, as the most popular time for pension top ups based on analysis of its customer’s behaviour across 2024 and 2025. Looking further back, this is consistent with top-up peaks in 2022 and 2023.

This annual spike, beginning in late February and peaking at this point in March, reflects the focus many people place on maximising their allowances and strengthening their long-term financial security.

Inflows into Standard Life pensions by week of the year:

Mike Ambery, Retirement Savings Director at Standard Life plc, said: “A lot of attention goes to ISAs at this time of year, but it’s encouraging to see people are also making the most of pensions – one of the most tax-efficient long-term savings tools available. With allowances resetting on 5th April, the weeks leading up to tax year end are a crucial window for many savers, and our data shows a clear shift in behaviour as people look to top up before those opportunities reset.

“Everyone’s journey to and through retirement can be better, and even small pension top-ups can make a meaningful difference over time thanks to the potential power of compound investment growth - helping to build lasting financial security. Tax relief adds an extra boost by increasing the value of what goes into your pension from day one, making every contribution work harder for you. For higher- or additional-rate taxpayers, the ability to reclaim extra relief can make these end-of-year top-ups particularly efficient.

“For anyone with income near thresholds like the personal allowance taper or the child benefit charge, contributions made now can also help reduce the amount of tax you pay this year while strengthening your long-term financial wellbeing at the same time.”

Mike’s top tax year end pension tips

1. Make full use of your pension annual allowance – “Your pension annual allowance – the amount you can save into your pension each tax year while still receiving tax benefits – is currently the lower of £60,000 or 100% of your earnings. This includes contributions from you, your employer and third parties. Higher earners may have a tapered allowance, reducing to as little as £10,000 if adjusted income exceeds £260,000. You may also be able to carry forward unused allowances from the previous three tax years.

“If you’ve already accessed your pension, it’s important to be aware that the Money Purchase Annual Allowance (MPAA) may apply instead, reducing the amount you can contribute to £10,000 a year while still receiving tax benefits. This is triggered when someone begins taking taxable income from their pension, so it’s good to know which allowance applies to you.”

2. Top up your pension payments with tax relief – “Tax relief makes your pension one of the most tax-efficient ways to save for retirement. When you pay into your pension, you receive tax relief on your contributions - meaning the money you put in is effectively free of income tax. This boosts your pension savings at no extra cost to you.

“For example, if you’re a basic-rate taxpayer and pay £80 into your pension, the government adds £20 in tax relief, so £100 goes into your pension pot. “Most savers receive 20% tax relief automatically. Higher- and additional-rate taxpayers may be able to claim extra relief (to reach 40% or 45%) through Self Assessment. However, some people don’t need to claim anything because their scheme gives full tax relief through payroll - for example, via salary sacrifice or a ‘net pay’ arrangement, where contributions are taken before income tax is applied.

“It’s a good idea to check with your employer or pension provider to understand exactly how tax relief works in your specific scheme.”

3. Consider bonus sacrifice – “For those expecting a bonus, redirecting some or all of it into your pension can be a highly efficient way to strengthen your retirement savings. Bonus sacrifice can result in savings on Income Tax and National Insurance, making it a smart way to keep more of the value of your reward while giving your pension a meaningful boost. It’s a straightforward step that can help your money go further - just be sure to check that your total contributions remain within your annual allowance.”

|