In a world that feels increasingly complicated, uncertain and unpredictable, people are thinking differently about how they’ll fund life after work. Rather than relying on a single source of income, new research from retirement specialist Standard Life shows that younger generations are more likely to expect a combination of pensions and property to underpin their financial security in later life – while older generations are more inclined to rely on pensions alone.

More than one in three Millennials (35%) and Gen Z (39%) expect to use a combination of pension savings and property to fund their retirement. In contrast, a quarter of Baby Boomers (25%) and just one-in-five of Gen X (21%) expect to follow this combined approach, with half of Baby Boomers (50%) and over half of Gen X (52%) instead favouring a total reliance on pensions.

Economic realities are reshaping retirement expectations

People across all age groups are grappling with higher living costs and greater economic uncertainty, but the impact is being felt in different ways across the generations. Many younger adults are juggling more immediate financial pressures – from rent and mortgage payments to day-to-day living costs – which can push long-term retirement planning further down the priority list. Against that backdrop, relying on a combination of pensions and property can feel more realistic than betting on a single route to later-life security.

Gen X workers in the private sector largely missed out on the full benefits and security of Defined Benefit pensions and property may help bridge the gap. Three quarters (75%) already own their home, either outright (38%) or with a mortgage (37%), giving many a valuable source of longer-term resilience alongside pension savings. Baby Boomers and older generations, by contrast, are more likely to own their home outright (78%) and benefit from DB pensions (42%, compared with 28% of Gen X) – factors that can provide greater certainty over retirement income and naturally shape more pension-led expectations.

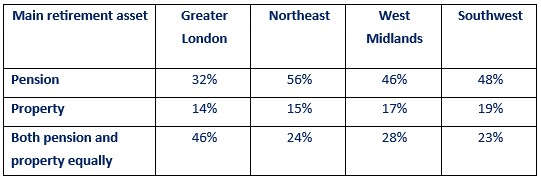

Regional differences reveal divides in how people view pensions and property

Standard Life’s research also highlights clear regional differences in how people view their path to retirement income. In the Northeast, more than half (56%) expect to rely mainly on a pension, compared with just under a third (32%) in Greater London. London stands out for its far higher proportion of people who see pensions and property as equally important (46%), while reliance on property alone remains relatively low across all regions.

Commenting on the property vs pension debate, Mike Ambery Retirement Savings Director at Standard Life plc, said: “Younger generations are coming of age in a very different financial landscape to those before them. Many face higher living costs, less predictable career paths and far greater barriers to getting onto – or moving up – the property ladder, while also being far less likely to benefit from the certainty of Defined Benefit pensions. Against that backdrop, it’s no surprise that many aren’t putting all their hopes on a single route to funding life after work.

“Everyone’s journey to and through retirement can be better, and that starts with acknowledging how people actually live today. For younger generations, that means recognising the financial pressures they’re under and focusing on simple, realistic steps they can take now – even if the long-term goal still feels a long way off.

“Whatever your age or stage in your journey to retirement, small, consistent pension contributions remain one of the most reliable ways to build long-term financial security. And with attitudes on retirement assets varying so sharply across the UK, it’s clear that where you live can also shape how you think about building that stability – whether that’s feeling more reliant on pensions in some regions or taking a more blended approach in others.

“For many, property can be a key financial asset when it comes to funding later life, but it’s important not to overlook the attractive features and tax advantages that come with a pension. The aim is to feel more confident and in control of your future by taking manageable steps that strengthen your financial foundations over time.”

|