By Sarah Vaughan, Director at Angelica Solutions

Claims data gets sliced and diced into different claim types, claim counts (with and without nil claims), propensities, third-party intervention, large claims, small claims; the list goes on. All of this is then combined with every scrap of policy and customer behaviour data in order to try and quantify the relationship between what an insurer knows at point of quote and the claims that will ultimately get paid.

Then we get to the final piece in the puzzle, getting the level of prices right. Very early in my career, in my first in-house role as a Head of Pricing, an experienced underwriter I met during the obligatory meet and greet said to me, ‘I understand all this new [at the time] theory of building Generalised Linear Models (GLMs) of claims data but tell me, how do you go about setting the base rate?’.

As a newly qualified Actuary, I thought there was an easy response and proceeded to rattle through the stock exam question answer about reserving ultimates, claims inflation and average claims occurring halfway through a policy year etc. Now, nearly 20 years on, I find myself reflecting on this question regularly and realise that the individual in question was on to something. It isn’t easy to get the level of the rates right.

My experience of executing this in reality is that the textbook answer has in fact been one of regular disconnect between the land of Pricing and the land of Reserving, meaning that what sounded like an elementary case of multiplication, turns into layer upon layer of assumption, interpolation, adjustment and inference. At best this costs time but at worst it makes a serious dent in underwriting performance.

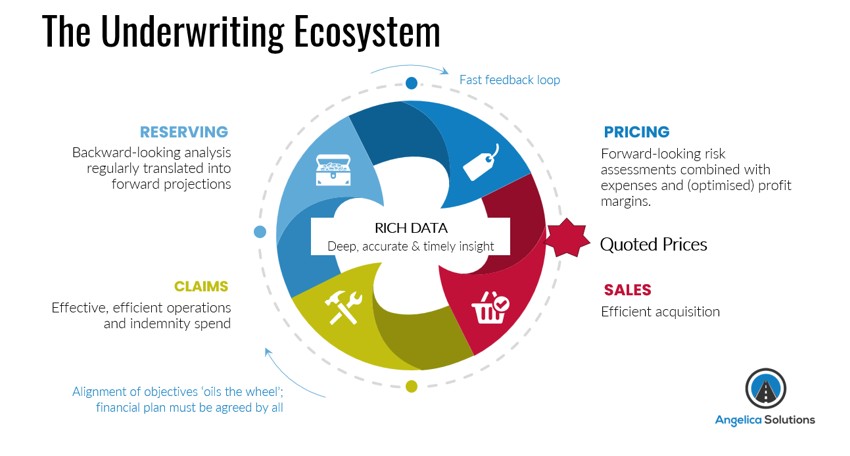

These challenges persist despite, and in some cases because of, the relentless march forward in modelling sophistication. Pricing and Reserving teams often work from subtly different versions of the same reality, whether through differing claim type definitions, data exclusions, claims capping levels or aggregation structures. Claims and policy data may not reconcile across source systems, catastrophe models may be built around geographic regions that do not align with pricing structures, and even seemingly straightforward issues such as currency conversion can introduce additional layers of adjustment. Differences in time horizons and projection methodologies, such as monthly versus annual views or accident year versus underwriting year analyses, add further complexity, while the frequency and timeliness of reserving updates do not always match the pace at which pricing decisions need to be made.

Overlaying all of this are the challenges of separating exceptional events from underlying performance and reaching a consensus on future claims inflation, meaning that what appears on the surface to be a simple feedback loop often becomes a process of interpretation, adjustment and judgement.

In the interests of balance, the challenges do not all flow in one direction. Changes made by Pricing teams can create significant difficulties for Reserving too. Shifts in the mix of business may mean that changes in average premium are not proportionate to changes in underlying risk, while updates to underwriting rules or acceptance criteria may not be fully captured by even the most sophisticated risk indices. Product and coverage changes can alter expected claims costs, and changes in business mix can influence the balance between claim types, reporting patterns and settlement rates in ways that are often difficult to quantify with confidence. To compound matters further, reserving data is not always available at the level of granularity needed to isolate and adjust for these effects, making it challenging to separate genuine performance changes from the consequences of evolving business strategy.

In many larger insurers, Pricing and Reserving sit in separate functions. This separation brings important governance benefits and helps avoid situations where teams are effectively marking their own homework. However, separation can also create distance.

Pricing teams often need answers at a pace that traditional reserving cycles struggle to support. It is not uncommon for pricing decisions to be informed by reserve reviews that are already several months old before they reach the people who need them. By the time any differences in peril definitions, large-loss treatment or data structures have been reconciled, valuable time has been lost.

Meanwhile, smaller insurers, MGAs and brokers often operate with leaner teams where individuals wear multiple hats. Although they may not always carry direct loss ratio accountability, many still have profitability-linked remuneration structures that make understanding underlying performance just as important. The challenge, therefore, is not simply one of communication between Pricing and Reserving. It is about ensuring that reserving processes have evolved to meet the needs of modern insurance businesses.

Over the last twenty years, pricing functions have undergone a transformation. They have embraced richer data, greater automation, more frequent monitoring and increasingly sophisticated analytical techniques. Reserving has also evolved, particularly in response to regulatory requirements around capital, variability and solvency, but there remains significant opportunity to increase speed, agility and operational value.

Modern reserving should be rapid, friction-free, informed, consistent and granular, combining automated analysis with near real-time data and alignment to pricing assumptions. This enables insurers to identify emerging trends sooner and make better-informed decisions. Ultimately, the objective is not to blur the lines between Pricing and Reserving, but to ensure they are working from the same version of reality. The closer the alignment between the two functions, the more effectively an insurer can understand performance, respond to emerging trends and make informed underwriting decisions.

|