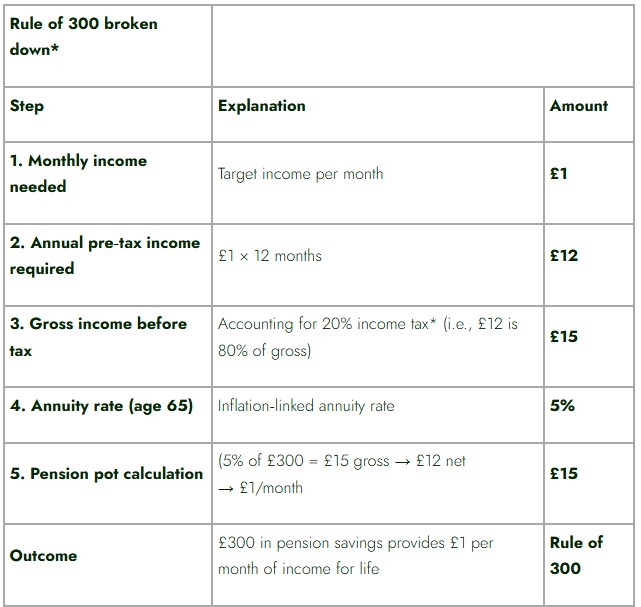

A rule of thumb called the “Rule of 300” gives households a straightforward way to gauge how much of their pension pot they will need to cover everyday expenses for life, to and through retirement. This is according to calculations from Standard Life; a retirement specialist focused entirely on retirement savings and income.

Based on current inflation-linked annuity rates for a healthy 65-year-old (4.99%), retirees need around £300 of pension savings to secure £1 of guaranteed monthly income for life. This means multiplying any regular monthly cost by 300 reveals the pension savings needed to secure it for life. And because an inflation-linked annuity protects income against rising prices, the Rule of 300 helps people understand these costs in real terms, not just today’s prices.

By using everyday examples it’s possible to see how common monthly expenses convert into the pension savings required to fund them for life. For instance, a typical £12 per month streaming subscription would require around £3,600 of pension savings, while a £30 per month broadband bill equates to roughly £9,000.

Everyday examples using the Rule of 300

Typical streaming subscription (£12/month) → £3,600 needed

Mobile phone contract (£25/month) → £7,500 needed

Broadband (£30/month) → £9,000 needed

Average gym membership (£50/month) → £15,000 needed

Average golf club membership (£75/month) - £22,500

Car (£3,500/year) → £87,500

* The Rule of 300 uses a 20% income tax assumption for illustration. Actual tax treatment will vary based on individual circumstances

Pete Cowell, Head of Annuities at Standard Life said: “The Rule of 300 turns retirement planning into something real that people can relate to. It shows, in simple pounds and pence, how everyday monthly costs translate into the pension savings needed to cover them for life.

“Too often pensions feel abstract. By linking retirement income back to familiar bills and subscriptions, the Rule of 300 helps people picture what their pension really needs to deliver, and plan with much greater confidence.”

Comparison with 4% drawdown rule

Although the Rule of 300 is derived from annuity pricing, it aligns broadly with the 4% drawdown rule, which suggests retirees need around 25 times their annual spending in pension savings. Both rules reinforce the same message: planning and budgeting are critical, regardless of the retirement income route chosen, and clearer tools help more people engage earlier and more confidently with their long-term financial futures.

However, the risks differ as drawdown income depends heavily on investment returns and withdrawal behaviour. Previous Standard Life analysis shows that a £100,000 pension could last a lifetime if withdrawals stayed at £4,000 annually, and investment growth remained over 5%. However, it could run out in just 13 years if withdrawals were higher and returns lower depending on market performance and income levels, underlining the challenge of making savings last throughout retirement.

Pete continued, “Understanding your day-to-day spending is one of the most important parts of retirement planning. The State Pension will cover some core costs, but for most people it won’t stretch to everything they want or need in retirement.

“Whether someone uses an annuity, drawdown, or a combination of both, being clear about essential spending can make a real difference to long-term financial security. If people need support, getting guidance or speaking to a financial adviser before making major retirement decisions can really help.”

|