Against a backdrop of rising living costs and continued market uncertainty, we are seeing an emerging trend around “unretiring” according to research1 from the retirement specialist Standard Life, with a significant proportion of retirees heading back to work as the financial reality of retirement falls short of expectations. One in six (16%) retirees say they have either already returned to employment (8%) or are considering doing so (8%).

While some have returned or are considering returning to work by choice, with a quarter (24%) saying they feel lonely or socially disconnected from others when not working, the findings highlight that financial pressures are a key driver behind this ‘unretirement’ trend. Almost a third (30%) of retirees say their standard of living is worse than before they retired, compared with just over a fifth (22%) who say it is better.

Many also feel underprepared for retirement. A fifth (20%) say they did not realise how much money they would need in retirement, with a similar proportion wishing they’d had planned their retirement more thoroughly (21%), and one in five (19%) say they had not appreciated how long retirement would last.

Retirees set to feel the impact of rising prices

Inflation has had a significant impact on retirees’ day to day spending. Analysis shows that £100 in 2020 is now worth just £78.25 in real terms2, meaning people’s spending power in retirement has been eroded over a relatively short period. For people who retire before state pension age, or who do not have a defined benefit pension with built-in inflation protection, maintaining income in later life can require more planning and, in many cases, greater investment risk.

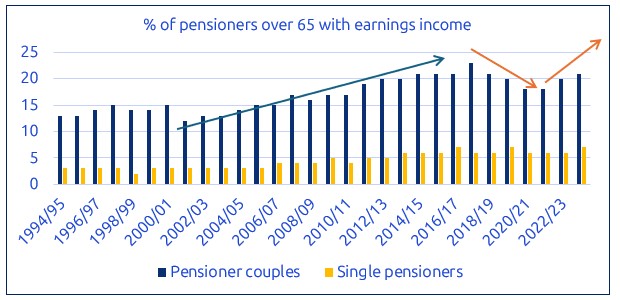

Recent DWP data3 shows that the proportion of over 65s with earnings income has been increasing in recent years and the trend is closely correlated with a period of higher inflation. Price rises have likely a factor in peoples’ decision making and will remain front of mind with the conflict in the Middle East setting expectations of further pressures on the cost of living.

Retirement is becoming more flexible, but challenges remain

With a longer-term perspective, expectations around retirement are shifting, with fewer people viewing it as a single, fixed moment when work simply stops. This change has been building for decades - from the early 2000s onwards, the proportion of pensioners receiving income from work gradually increased, reflecting a steady move towards working later in life or combining work with retirement.

That long-term trend briefly went into reverse during the pandemic, often described as ‘The Great Retirement’, when many older workers left the workforce earlier than planned. Since 2021/22, however, the proportion of pensioners with earnings income has begun to rise again, suggesting this was a pause rather than a permanent shift.

However, this evolving picture doesn’t come without challenges. While more than three-quarters (78%) believe they could still do their job at age 60, this confidence drops to around half (49%) by age 70. People point to potential barriers such as poor health (39%), the need to retrain or change roles (26%), and concerns about age discrimination (24%). Looking ahead, uncertainty remains, with more than a third (38%) expecting their retirement lifestyle to be worse than their current one - rising to nearly half of Gen X (49%) and over two in five women (43%).

Mike Ambery, Retirement Savings Director at Standard Life plc, said: “Retirement is no longer a single moment where work simply stops. For many people it’s becoming a more flexible journey, shaped around the life they want to live, and more flexible approaches to work – including part-time roles and phased retirement – are making it easier for people to stay in the workforce for longer and shape work around their changing needs later in life.

“For some, returning to work is about staying active and connected. But for others, it reflects the reality that retirement isn’t always turning out as expected, particularly as rising costs put pressure on incomes. In a world that feels increasingly uncertain and unpredictable, it’s more important than ever that people feel supported to engage with their financial futures and understand what their retirement could look like.

“Simple steps can make a real difference, whether that’s before or during retirement – from regularly checking in on your pension savings and thinking about how you’ll use them to generate an income, to reviewing how much you’re taking and whether it’s likely to last for the years ahead. It’s also important to check when you’re due to retire, as your planned retirement date and your State Pension age don’t always align, and to make sure you’ve planned for any gap between the two. Taking time to consider the kind of lifestyle you want, exploring phased or flexible retirement options, and seeking guidance early can help people make more informed decisions. Planning ahead means people are better placed to manage their money with confidence and achieve greater financial security over the long term.”

|