Life can be complicated and rarely involves a linear journey to retirement; instead it is shaped by pivotal moments that introduce uncertainty or make the future look unpredictable. New research from Standard Life, a retirement specialist focused entirely on retirement savings and income, shows that major life events frequently disrupt peoples’ ability to save for retirement. Over a third (37%) of UK adults who experience one and have a private pension say it led to them pausing, reducing or stopping pension contributions.

Taking a career break (45%), followed by redundancy (44%), becoming self-employed (33%), and after having children (21%) are among some of the most common triggers, according to the research, which explored key life moments and their impact on long-term savings. While retirement saving is often seen as a steady, long-term habit, the reality is that people’s financial lives rarely move in a straight line. Contributions often rise, fall or pause as people navigate the ups and downs of life – reflecting how people actually live rather than how the system assumes they do.

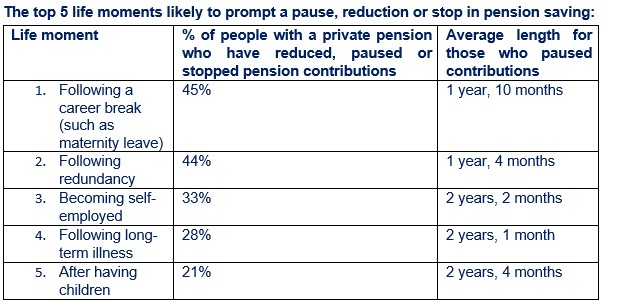

Career breaks are the most likely life event to impact peoples’ ability to save for retirement, with 45% of those who have experienced one saying it led them to reduce, pause or stop their pension contributions, with pauses lasting one year and 10 months on average. Redundancy follows close behind (44%) but notably has the shortest average pause, at one year and four months. This suggests that while redundancy is a common saving disruptor, many people restart contributions relatively quickly when they return to work – auto-enrolment is likely a welcome factor in this.

In contrast, one in five (21%) of people who have had children say this led to pausing, reducing or stopping contributions into their pension (with an average pause of two years and four months), as well as almost one in five (18%) of people who have caring responsibilities, – which suggests that life events linked to longer-term structural changes tend to result in longer contribution gaps, even if fewer people are affected overall. Certain groups – notably women and younger generations – feel the financial impact of life’s ups and downs more sharply

The impact of life events on pension saving is not evenly felt. Women, for example, are significantly more likely than men to pause, reduce or stop pension contributions after starting a family (27% compared with 16%).

Younger adults feel the impact particularly sharply, as nearly a third of all Gen Z (32%) and Millennials (33%) have paused or reduced contributions as a result of life moments, compared with 24% of Gen X and just 16% of Baby Boomers. Furthermore, becoming self-employed is also a major trigger for Gen Z pausing reducing or stopping their pension contributions (56%), as well as taking a career break such as maternity leave (59%), being made redundant (57%), having children (51%), and buying their first home (44%).

The long-term cost of a “temporary” pause

While the average pause following a major life event lasts two years, for a notable minority, the disruption becomes far more prolonged. One in seven (14%) of those who pause pension contributions did so for more than five years for at least one of the life events they have experienced – and Standard Life analysis shows how these longer breaks can have lasting consequences. Someone starting work at the age of 22 on a salary of £25,000 and pays the minimum monthly auto-enrolment contributions (5% employee, 3% employer) could build a retirement pot of around £210,000 by age 68, allowing for 2% inflation and charges2. However:

A two-year pause (around the average length people pause their contributions as a result of a life event) between ages 30 and 32 could reduce that pot to £200,000, £10,000 less

A five-year pause between ages 30 and 35 could reduce that pot to £185,000, £25,000 less

A ten-year pause between 30 and 40 could reduce it to £161,000, £49,000 less

A fifteen-year break between 30 and 45 could bring it down to £138,000 (£72,000 less).

Cause for optimism

Despite the disruption life events can cause, there is optimism about making up for lost time. Three in five (62%) people yet to retire, who have paused, reduced or stopped contributions due to a life event, feel confident that they can make up any shortfall on their pension contributions. Nearly two in five (38%) of those who paused contributions already have a plan in place to manage this, including intending to increase contributions as their income rises (32%) or expecting to work for longer (24%) to restore lost momentum. Importantly, not all life events lead to reduced saving. Nearly a fifth (18%) of those who started their own business say it led to them increasing their pension contributions, as did one in ten (11%) of those who have had children.

Mike Ambery, Retirement Savings Director at Standard Life plc, said: “Life rarely follows a straight line - and pensions don’t either. Life events such as being made redundant, managing long-term illness, starting a family, or taking time out are simply part of how people actually live, and it’s completely normal for retirement saving to pause during those moments. The challenge is that pensions build over decades, so even relatively short gaps can have a bigger impact than people expect. A pause might feel temporary at the time, yet it can have a lasting impact if contributions aren’t restarted. Everyone’s journey to and through retirement can be better, and the encouraging news is that small steps can make a real difference. Restarting contributions as soon as possible can help rebuild momentum. From there, gradually increasing payments when income rises, using part of a pay increase or bonus to boost pension contributions, and checking the full employer contribution available through a workplace scheme, can all help empower people to engage with their financial futures and help them get back on track to achieve better outcomes and greater financial security in later life.”

|