Withdrawing a pension in full can trigger unexpectedly large tax bills. Because the withdrawal is treated as income, it can push savers into a higher tax bracket in a single year. This means a significant portion of their retirement pot may end up going straight to the taxman.

The rise in people cashing in their pensions also comes as policymakers warn the UK faces a growing retirement savings gap. If more people are cashing their pensions in full, it suggests that increasingly the amount people have saved at the point of retirement simply isn’t big enough to offer meaningful income via drawdown.

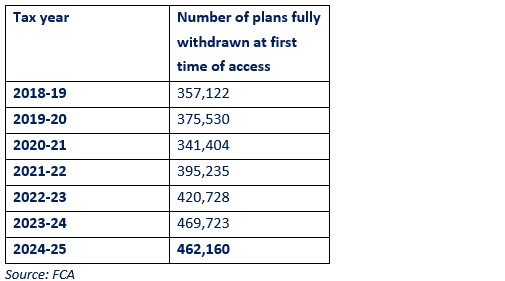

By pot size, more than 300,000 pension pots withdrawn in full in 2024-25 were worth less than £10,000, and a further 112,526 were worth between £10,000 and £29,000.

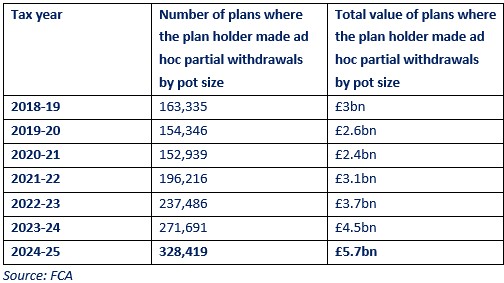

Ad hoc withdrawals have also increased. The number of pension plans from which an ad hoc partial withdrawal was made in 2018-19 was 163,335. In 2024-25, this had reached 328,419 – marking a 101% increase. These types of withdrawals can also incur large tax bills.

Looking across age brackets, there has been a 75% increase in 65-74-year-olds withdrawing their pensions in full between 2018 and 2025. For those aged 55 to 64, the rate of pensions being withdrawn in full rose by a lesser 15% over the same over this period.

Georgie Edwards, DC Proposition Associate Director at TPT Retirement Solutions, said: “The rise in people cashing in their pensions in full is a worrying signal about retirement adequacy in the UK. For many, it’s not a strategic choice but a sign their savings aren’t sufficient – and some may also be reluctant to consolidate pots, missing the chance to build a more sustainable income.

“In some cases, savers are stuck in legacy products that don’t offer flexible options like phased drawdown or regular UFPLS [Uncrystallised Funds Pension Lump Sum], effectively forcing higher withdrawals than they’d prefer and increasing their tax exposure. That’s particularly concerning because full withdrawals are taxed as income, often pushing people into higher tax brackets unnecessarily. It highlights the need for better guidance so retirees don’t erode their savings – or pay more tax than they need to.”

|