|

|

The Aon UK DC Pension Tracker rose over the third quarter (July to September) of 2022. This suggests that the expected future living standard in retirement provided by DC savings was higher than at the end of the previous quarter. As usual, this overall increase masks a more complex picture – and one particularly driven by expected returns rather than the reality of current markets. |

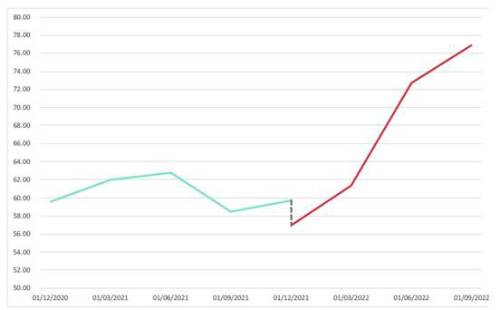

Aon UK DC Pension Tracker

Source: Aon UK DC Pension Tracker (1 July – 30 September 2022) Over the quarter, the tracker rose from 72.7 to 76.9. As with previous quarters, this rise is primarily driven by increases in expected returns, across all asset categories. Unlike previous quarters, if we ignore changes to the future return assumptions, the tracker would still have risen over the quarter as a result of positive benchmark equity returns. However, the increase in the tracker would have been less pronounced, to 73.1 rather than 76.9. This all suggests that our sample savers are, on average, expected to have a higher standard of living in retirement than was expected at the end of the previous quarter. However, the apparently benign picture for savers masks the fact that the Aon UK DC Pension Tracker is comparing against Retirement Living Standards that were set before the recent high levels of inflation. Making allowance for the rise in the cost of living is likely to mean the DC Tracker scores being substantially lower. Savers’ Positions

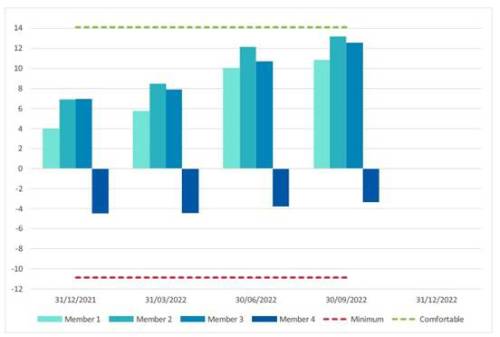

Source: Aon UK DC Pension Tracker (1 July – 30 September 2022) Expected outcomes improve but experience is mixed depending on age The third quarter of 2022 saw historic levels of volatility in bond markets, particularly at the end of September. This led to significant falls in the value of bond assets which are typically seen as being more ‘low risk’ and ‘safe’ in the run up to retirement. This reduced the expected retirement income for our older saver who has started to diversify into these asset classes as they approach retirement. Equity returns over the quarter were marginally positive which benefited all of our sample savers. Increases to the expected future return assumptions, across all asset classes, led to an increase in expected retirement outcomes, particularly for younger members.

Mixed position for savers If we consider the effect of investment performance in isolation over the quarter:

• the three younger members would be expected to be slightly better off in retirement due to increases in equity assets over the period. Based on this experience alone each of them is expected to be around • In contrast, the oldest member is expected to be around £150 per year worse off in retirement due to the fall in the value of their typically more ‘defensive’ bond assets. Increases to the expected future investment returns, across all asset classes, led to further rises and meant some of our sample savers are expected to be very close to achieving the existing ‘comfortable’ level of retirement living standard: • The youngest saver had an increase in expected income of around £750 p.a.. This was due to an increase in future expected returns over the period until retirement, which was offset by a decrease in the expected return they may achieve when they start taking their funds in retirement. • The 40-year-old saver saw an increase in their expected retirement income of around £950 p.a. for the same reasons. • Savers closer to retirement saw less of a reduction in the expected returns they could achieve when they start to drawdown their benefits in retirement. This meant the 50-year-old saver saw the largest expected increase over the quarter (of around £1,700 p.a.) when compared to the start of the quarter. • The expected income for the oldest saver increased by the smallest amount (around £400 p.a.) as higher future expected returns, both before and after retirement, were offset by investment return over the period. • Overall, the oldest saver is expected to be the worst off in retirement, with a retirement income slightly below the current moderate standard of living. This excludes any DB benefits they may have which are not included in this projection. • The younger three savers are all currently expected to achieve close to the current comfortable standard of living in retirement. Do your investments match your expected retirement choices? The third quarter of 2022 saw another period of high volatility for asset owners. In particular, unprecedented volatility in the UK government bond market has contributed to the continued weak performance of typical ‘lower risk’ asset classes. Short term volatility aside, 2022 has been a year where rising bond yields have caused poor performance across defensive asset classes, typically favoured by default investment strategies looking to protect older members against market shocks in the run-up to retirement.

The Aon UK DC Pension Tracker is based on sample members who are invested in a typical ‘drawdown Savers are at particular risk when their investment strategy approaching retirement fails to match their expected retirement choices. Any savers invested in an annuity-focused lifestyle strategy but planning to take their benefits through drawdown, will be looking at a much smaller retirement fund from which to draw down. They will also have unpalatable choices of increased investment risk, a lower income in retirement or potentially even having to retire later. Matthew Arends, partner and head of UK Retirement Policy at Aon, said: “Given the overwhelming majority of DC savers invest in a default fund, trustees should be considering whether their existing lifestyle strategies, and particularly the default investment strategy, are appropriate for their membership. They may also want to consider whether they should be doing more to engage with members over their expected retirement choices and investing accordingly. “Savers should also be reviewing their investment choices, particularly where they have multiple DC pension pots from previous workplaces, which often can be forgotten about or not considered as frequently as their current pension.”

Glut of early retirements - but can it last? Matthew Arends said: “The current trend of early retirement is undoubtedly complex to unpack but we expect the majority of those leaving the workforce to have significant defined benefit pensions. As the majority of employees in the private sector are now building up defined contribution savings, there may be a limited window where savers with legacy defined benefits pension can afford to retire early while their peers with DC benefits only, remain in the workforce.

“This trend could however lead to a change in retirement expectations and the way people access their retirement savings. There may be an increase in members accessing their DC savings in their 50s while continuing to work, potentially part-time or in a different career.” |

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd