BENEFITS OF DIVERSIFICATION

Theoretically, however, it’s quite valid- if an asset class offers meaningful diversification, is there a case that it should be a part of every portfolio where there are no explicit reasons to exclude it, rather than only part of those where there is an explicit reason to include it?

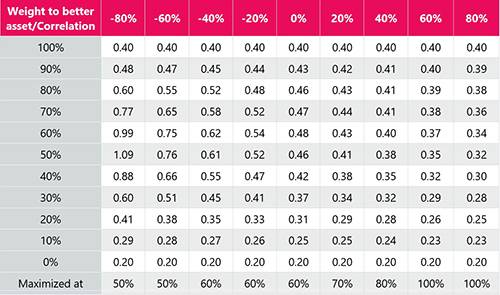

As a simple example, suppose there are only 2 assets available. Both are lognormally distributed with 10% volatility, but one has a 4% return and one has a 2% return. What Sharpe ratio do you get from different portfolios depends on the correlation between them, as shown below:

Even with a much lower return, the second asset still justifies a place in the portfolio unless it is highly correlated with the first. If the correlation is negative, even an asset with a negative return can improve the Sharpe ratio- a 20% allocation to a -1% return asset would improve the Sharpe ratio even when the higher returning asset had a Sharpe of 0.4.

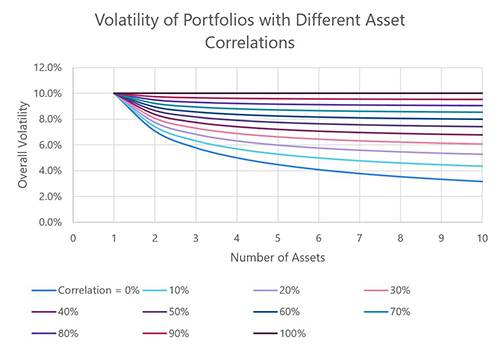

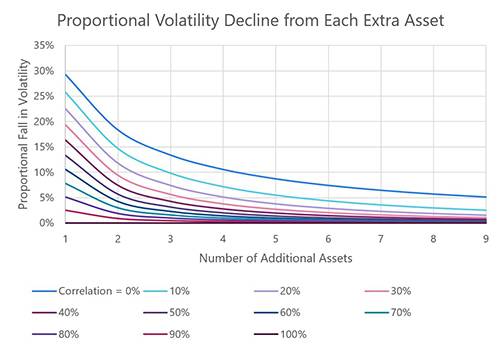

This benefit is somewhat limited- the marginal value of increasing diversification decreases, and it doesn’t take long to reach a point where the decline in diversification is within margin of error. This is especially true when the assets are reasonably positively correlated, which is increasingly likely as you add asset classes to a portfolio. The charts below show this effect for equal weighted portfolios with different numbers of assets at different correlations (each asset is assumed to have a 10% volatility).

In practice, there are a host of other considerations, not least governance, that will and should have a significant effect on portfolio construction. There are some cases where a portfolio should be concentrated- for example, if it is aiming to beat a benchmark, is part of a wider allocation, or is very small and constrained. However, as a rule of thumb, if there are fewer than 3-4 meaningfully different sources of returns in a portfolio, it may be worth looking at increasing diversification.

|