By Alistair Russell-Smith, Partner & Head of Corporate DB at Hymans Robertson

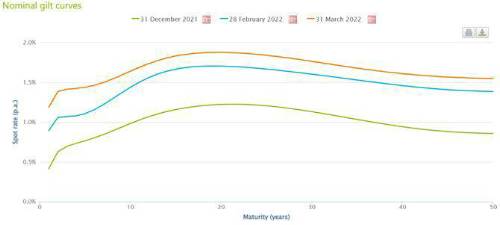

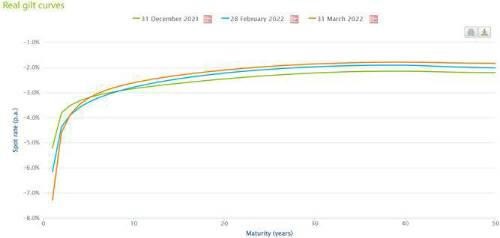

On the liability side, there have been significant rises in nominal and real yields over the year, as can be seen from the yield curve movements below. This is positive news for DB funding. Even schemes that have hedged interest rate and inflation risk tend to leave the deficit unhedged, meaning these rises will have reduced deficits in £ amount terms.

So funding levels are healthy right now. We estimate the aggregate (IAS19) funding level of the FTSE 350 was 118% at the end of the first quarter (up 3% from year-end and up 6% from an early March low). But the Ukraine crisis has clearly introduced a significant increase in downside risk. Rising oil and gas prices could further increase inflation and restrict global growth. Higher commodity prices could weigh on European growth and squeeze corporate profit margins, putting European equities at risk of underperforming other regions.

With this increased downside risk, we think that corporates should consider the following actions in relation to DB funding:

If you're in the middle of a triennial valuation process, get on and agree it. With an increased risk of a downturn in funding, it is better to lock in contribution schedules sooner rather than later. Companies with valuation dates between 31 March 2021 and 31 December 2021 should be looking to finalise valuations as soon as they can.

If you're considering de-risking the investment strategy, again get on and do it. Real yields were up 40bps and nominal yields were up 70bps in Q1 2022 with further increases after the quarter end, and equity markets are broadly flat – this doesn’t feel like a bad time to be taking off some investment risk and increasing hedging, particularly if there's a planned programme to do this over time anyway or if your valuation package is predicated on scheme funding staying at current levels.

|