|

|

The concept of “financially material” risks, and whether you can take actions to deal with them, has never been more relevant. That makes your life hard as a pension scheme trustee. We firmly believe systemic risks are financially material; we all need to manage them better than we do currently, to protect our economy, our schemes and our members. |

By Tom Fieldsend, Consultant and Jacob Shah, Partner at LCP No doubt having read the call to action in Jacob’s article, you’re here to find out what you can do. I’m going to keep you in suspense for a little longer, as before we dive into the thick of the actual actions you can take, we have to consider the context that makes these actions appropriate. As with all good decisions, it's about finding a solution that strikes the right balance across what’s likely to be a number of considerations. I think too many decisions run the risk of being hyper-focused on short-term objectives, and can therefore ignore or forget about the longer-term outcomes and consequences. Consider climate change as an example. If you model the impact of warming scenarios on your funding position, an objective-driven model could well conclude that the best possible scenario is rapid global warming well in excess of 4 or 5 degrees. If the planet is uninhabitable, there won't be any surviving pensioners and therefore no pensions to pay. Therefore, your funding level will improve considerably; it'll probably go well past 100%! Your funding objectives have been achieved, but (clearly) the outcomes for members are, well, not so good. As a pension scheme trustee, you're a stakeholder in the pensions insurance regime, and could be involved in consultations on the solvency rules applicable to that market. With just your buy-out objectives in mind, you want better pricing to achieve the cheapest transaction you can. One way to achieve this would be to lobby for much laxer regulation. However, this would weaken not only the insurance system but threaten the whole financial system. With systemic risks in mind, ie. using a systems mindset, an individual scheme or stakeholder might choose to argue against their own immediate short-term objectives because it facilitates a better long-term outcome.

So, what actions can you actually take?

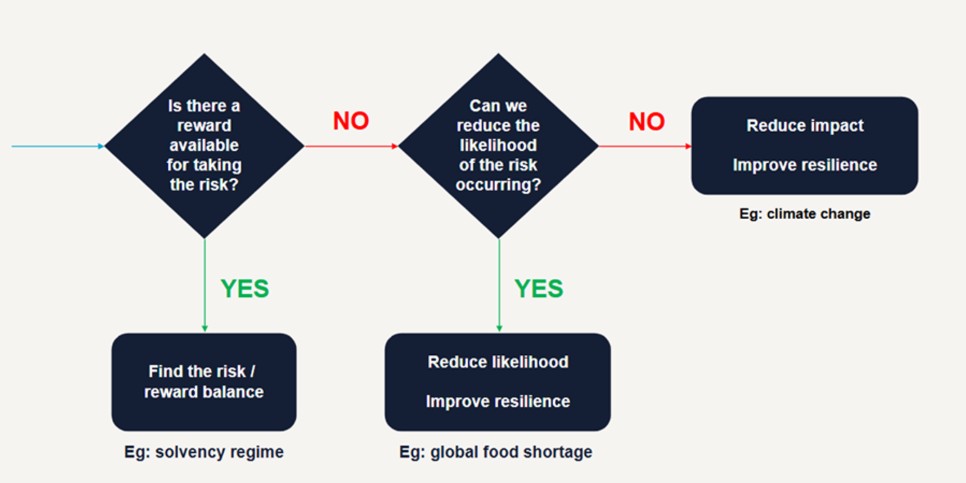

Evaluate As we look under the hood of each area you’ll see that there are tangible actions you can take, all of which can interact with each other, highlighting the integrated nature of the systems mindset.

Evaluate Some systemic risks we need to embrace, rather than remove entirely, since the offer upside as well as downside. Think back to the insurer solvency example above: if you just seek to enforce the strongest possible regime, removing as much of the risk as possible, then buy out essentially becomes unaffordable for everyone. This defeats the point of having the system in the first place. Climate change is an example of another type of systemic risk. To my mind, it’s different to other such risks in that it’s not a case of if it will happen, but how and when it will emerge. In this situation, our focus is going to be on stopping it from getting worse, mitigating its impact and best protecting our scheme and members. My final example are systemic risks of a more uncertain nature – there's no upside to them and we don't know which will occur. A global shortage of food is a good example here. We can potentially work to reduce the likelihood that these risks do materialise though; that should be the first focus. We do still have to be as resilient as we can as they could still happen (in fact almost certainly at least one will happen!); so we should work to protect the pension scheme as best we can from the impacts.

Clearly, it’s not quite this simple in practice. There is some interaction and overlap between types of risk, but these are some good examples to illustrate that there is more to think about than a “one size fits all” approach for addressing systemic risks. We've worked with a number of our clients on their investment and their ESG beliefs, which is a great place to start as it allows you to start building an understanding of the risks and the impact. When it comes to evaluating your risks, prioritise understanding them, this should enable you to write down your plan.

Advocate For those that haven't come across it before, we think of policy advocacy as using your voice to argue for and promote certain actions or policies from stakeholders, including governments and regulators. Given the capital they control, pension schemes have significant influence. If we as a group want to see change, we need to be proactive, making noise about what we want to see happen. Change doesn't happen automatically, it happens through evolution (or revolution) in societal thinking, which can lead to radical policy moves. Sometimes change happens because people put a hand up and fight for it. Communicating with investment managers on systemic issues or responding to relevant industry consultation are examples of policy advocacy. You can read Sapna Patel’s blog on best practice principles when doing this.

Collaborate Let’s consider the England men’s football team (stay with me here). When they go out onto the pitch, their objective (believe it or not) is to win the match. Each player will have their own idea of how to play their part in achieving that objective: Jordan Pickford will want the team to prioritise not conceding; Harry Kane will want lots of passes and crosses, so he can score as many goals as possible; and inevitably a controversial VAR call will mean we don’t talk about what any of them actually did anyway! Ultimately, if each player follows their own idea and their own objective, the chance of achieving the win is significantly lower than if they work together, with a clear plan to achieve that shared objective. You may well have responsibility for your scheme(s) and your members, but your aims are ultimately the same as those of other schemes and other trustees: achieve the best possible outcomes for those members. While some of you might be Harry Kanes and some of you might be Jordan Pickfords when it comes to navigating your scheme’s journey, you are all trying to get to the same place. You don't all need to agree on everything, but working together is going to make it far more likely you all achieve that objective together. Pooling your influence and advocating with a clear voice makes it far harder for other stakeholders to ignore you. Once you have enough capital behind your arguments, that HB pencil starts to look a lot more like a cargo ship; it starts to have a real world impact. LCP’s clients are increasingly taking part in multi-party advocacy, such as signing global investor statements and endorsing LCP’s climate policy asks. Collaboration could even be as simple as talking to another trustee about their scheme to find out what they’re doing. Is it something you could do too, or even something you could do together?

Mitigate

Outward-focussed mitigation: what effect can I have on the system?

Inward-focussed mitigation: what effect does the system have on me? “Being impacted” and “having an impact” are sometimes sensitive areas when it comes to pension schemes and fiduciary duty due to the association with financially non-material factors. The recent guidance Jacob referred to in Part I (the General Code, the DB Funding Code and the Financial Markets Law Committee report) all explicitly reference systemic risks. The FMLC paper even states that impact investing could be used, if the risk and return is properly considered. Properly addressing systemic risks absolutely belongs as a part of that consideration. When I was a child, one of my parents’ favourite books to read us was “We’re Going On A Bear Hunt”; a book where the protagonists want to see a bear, so they go searching for one. On their journey they come across many obstacles, such as long grass, a (swirling whirling) snowstorm, and thick oozy mud. There is a common theme to these obstacles: they can't go over them, they can't go under them; they have to go through them. As Jacob explained in Part I, you can’t avoid systemic risks. When they happen, they happen to you. You have to go through them. For your sake and for your members’, you should make sure you’re prepared, part of which involves having a systems mindset in place. That gives you and your members the best possible chance at a good outcome. There are a lot of possible actions laid out above and some of them will take work. If you want that easy win, if you want to take that next small step, if you want to start somewhere: allocate time. Give systemic risks the space they need on your agendas and in your priorities to become an integral part of your scheme management process. That is why we as consultants are doing all we can to find the right solutions and actions; why I have spent my Tuesday afternoon finding the perfect(ish) sports metaphor to make my point; why we spend our time fighting to put systemic risks into the pension scheme mainstream. We have allocated time, and we call on you to start by doing the same.

Key conclusions |

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd