|

|

As more pension schemes enter their endgame, defined benefit (DB) superfunds are emerging as a compelling alternative to traditional bulk annuity insurance transactions. Market confidence in DB superfunds has been boosted by five high-profile transactions completed by Clara Pensions. Clara’s recent transaction with the Church Mission Society Pension Scheme, in particular, has demonstrated how making use of a ‘connected covenant’ structure can open up the market to a broader range of schemes than was previously thought possible. |

By Jack Sharman, Principal and Senior Consulting Actuary, Barnett Waddingham

With the likelihood of more transactions from Clara, along with recent confirmation from The Pensions Regulator (TPR) that multiple organisations are actively discussing an entry to the superfund market, it is already shaping up to be a busy year in this space. This comes against the backdrop of the Government’s new permanent regulatory regime for superfunds, which should provide support for further market growth.

As the superfund market enters its next phase, with multiple providers expected to compete for transactions, two key questions naturally arise:

How big is the potential market opportunity?

How will a ‘mature’ superfund market operate alongside established bulk annuity providers?

Reviewing the potential market opportunity

Estimates of the potential size of the superfund market have varied widely across the industry. Different commentators have cited figures ranging from those implying a small market serving only schemes in a ‘niche’ set of circumstances, to those consistent with a material share of the overall UK DB universe. We set out below a transparent, data-led assessment of the potential market opportunity, based on our detailed understanding of current TPR guidance and the eligibility criteria that schemes will have to meet before transacting with a superfund. We have used data from a range of sources including the PPF ‘Purple Book’, TPR’s Scheme Funding Analysis and our own client base.

Our analysis suggests that while the current addressable market may be relatively modest, expected changes to market structure could expand it materially – potentially to around £180bn of DB assets.

The key criteria we have used to assess eligibility are:

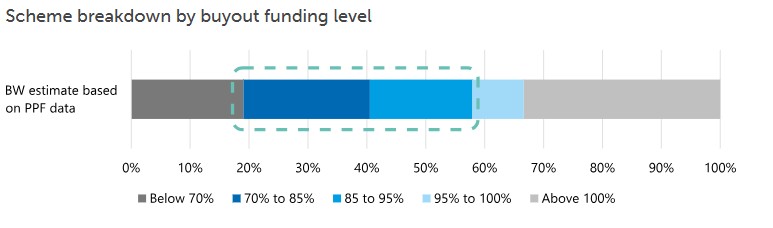

1. Buyout funding level

As at 31 March 2025, the DB pensions market consisted of around 4,800 schemes and £1.1trn of assets. The long-established ‘gateway’ principles set out in TPR’s guidance mean that superfund solutions are only likely to be relevant for schemes with a funding level strong enough for a superfund transaction to be affordable, but not so strong that benefits can be secured with an insurer in the short term.

Although there will inevitably be special circumstances that apply for some schemes, a good starting point might be to consider schemes with buyout funding levels in the range 70% to 95%. Schemes below 70% would likely be dependent on a prohibitively large sponsor contribution to be realistic, while those above 95% are likely to be assessed as too close to buyout to meet TPR’s gateway principles.

Using PPF data, we estimate that approximately 35% of schemes fall within this target funding range, as shown in the chart below.

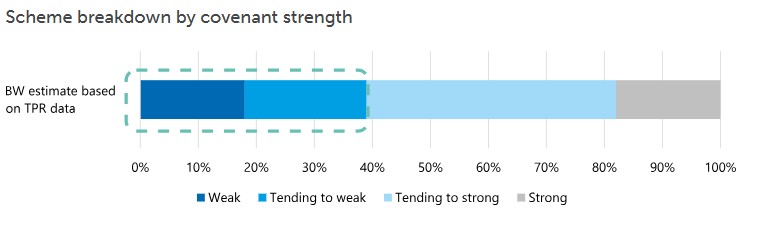

2. Covenant strength

A standard superfund transaction will result in the existing employer covenant being replaced by a finite pool of investor capital. This means that superfunds are naturally expected to be a more attractive solution for trustees of schemes with weaker covenants.

Using TPR data, we estimate that around 40% of schemes might have covenants which are sufficiently weak to make superfunds a natural fit.

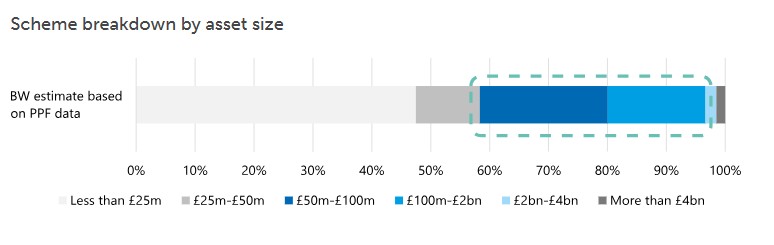

3. Scheme size

Based on current provider appetite, we expect the typical target scheme for superfunds to have assets of between £50m and £2bn. Using PPF data, we estimate that around 40% of schemes, with aggregate assets of £380bn, fall into this group.

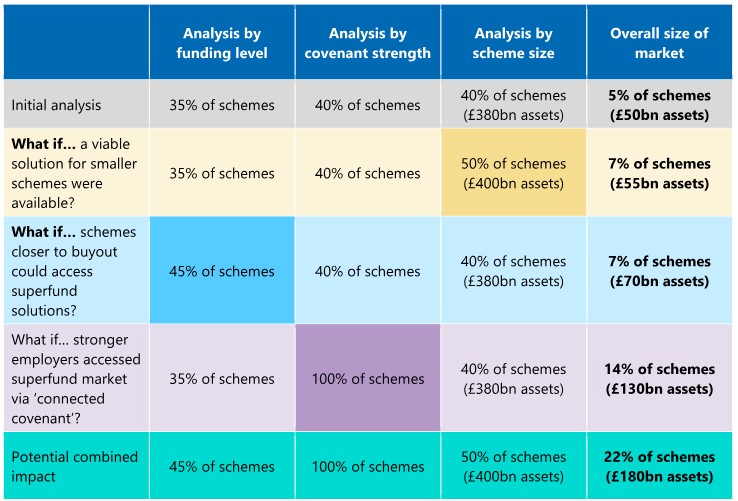

Taken together, and looking at the overlap between the three criteria above, an approximate starting estimate for the total DB market which might be served by superfunds is around 5% of schemes, equating to c.£50bn of assets.

The impact of recent developments

Recent changes to the dynamics of the superfund market should help to support further growth. In particular:

Streamlining of transaction processes, and the development of specific solutions for smaller schemes, could mean that superfunds start to open up to schemes with less than £50m of assets. Reducing the assumed minimum transaction size further to £25m would add a further 2% of schemes, or c.£5bn of assets, to the superfunds’ target market.

The simplification of TPR’s existing gateway framework, as proposed in the forthcoming Pension Schemes Act, means that some schemes which are closer to buyout may no longer be excluded from superfund transactions. Making superfunds available to schemes all the way up to full buyout funding would add around 2% of schemes, or £20bn of assets, to the market.

The increased familiarity with superfund models, and the development of novel solutions such as Clara’s ‘connected covenant’, may mean that these transactions are no longer limited to the weakest employers. If covenant strength were no longer a driving factor in determining the suitability of superfund solutions, this would add around 9% of schemes, or £80bn of assets, to the market.

Taken together, these developments point to a potential step-change in market scale. Under a more permissive and mature framework, superfunds could ultimately serve around 22% of schemes, covering approximately £180bn of DB assets, as shown in the table below.

This shows there is potential for significant growth in the superfund sector, and explains why multiple prospective providers and their capital backers have been keen to explore opportunities. The market opportunity could be even larger if, for example, schemes with above 100% buyout funding levels or more than £2bn of assets were included.

How might a mature superfund market operate?

For the past few years, Clara has been operating in a market of one. It is possible (if, for example, TPT is successful in completing its regulatory assessment process) that we will soon have multiple operational superfunds, each seeking to issue quotations and pursue the same transaction opportunities. In this environment, trustees and sponsors will need to make nuanced choices about which superfund solution best meets their objectives.

There are several factors that may be key to decision-making, including:

the providers’ regulatory status and track record of executing transactions;the providers’ investment strategies and pricing dynamics;

the ability to accommodate complex features that might traditionally present an obstacle to transactions, for example non-standard benefits or illiquid assets;

the likelihood of members and/or ceding sponsors sharing in any upside investment performance;

the intention (or not) of the superfund provider to ultimately secure liabilities in the insurance market; and

quality of administration and member experience.

In practice, different stakeholders are likely to place varying weights on each of the above considerations. We also expect to see more examples of schemes seeking quotations from both superfunds and one or more insurers. Our experience of running these multi-provider processes has shown they work particularly well when:

the process is run with a high level of transparency for all participating providers; and

all parties agree in advance to a framework for assessing quotations. This includes agreeing the relative weightings to be put on price and other factors such as member protections and outcomes in upside and downside scenarios.

Rebecca Whitehead, Actuarial Consultant, contributed to this article.

|

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd