|

|

Following the publication of the Financial Conduct Authority (FCA) policy statement on general insurance pricing practices , it is clear that a deeper understanding of the customer will be critical in this new regulatory environment and will almost certainly demand a much more granular level of risk assessment as part of the renewal process. |

By Martyn Mathews, Senior Director of Personal and Commercial Lines, LexisNexis Risk Solutions The new pricing regime will impact all corners of the market - direct insurers, intermediated insurers, large and small brokers. Based on a benchmarking exercise we undertook at LexisNexis Risk Solutions, each segment of the market could be impacted to varying degrees and have different considerations when ensuring they deliver fair value to their customer at renewal. Analysis of over 200 million insurance quotes per day has uncovered noteworthy variations in customer age profiles, retention levels and risks for these four key segments of the market.

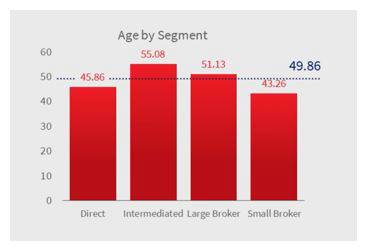

50 is the average age of a personal lines insurance customer In contrast, those who buy their insurance through an intermediated insurer tend to be slightly older at 55, but that is a 10-year difference on those buying direct, who are on average 45 years of age.

Direct Insurers cover more named drivers Just 35 percent of their motor books of business have no named drivers on a policy, while 21 percent have two or more. For smaller brokers, 52 percent of their motor book is main proposer only and just five percent have two or more named drivers.

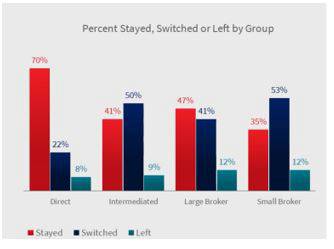

Named drivers pose an additional risk to insurance providers and can also create fraud risks such as fronting and ghost broking. The analysis highlights the importance of validating the identity of named drivers to the same level as main proposers. LexisNexis Risk Solutions identified that the average switching rate across all the segments’ motor insurance books is 32 percent. However, for direct insurers specifically, just 22 percent of customers switched their policy at renewal compared to 53 percent of the customers of small brokers. Direct insurers also have a 70 percent retention rate and the lowest rate of cancellations for the whole of the market.

25% have stayed with the same insurance provider for over 5 years. This insight is highly valuable as the market adjusts its pricing practices in-line with the new FCA pricing rules, particularly at renewal. Building a holistic view of existing customers’ needs is a good starting point. This can be done by leveraging a unique identifier such as LexID® that connects existing customer data to provide a single customer view. Approaching policy renewal, insurance providers will want to identify customers shopping around to support pricing consistency and retention strategies. This is where having a unique identifier for each customer brings further value as it enables existing policyholders to be flagged during the quote process. Quote behaviour data brings a further dimension to the understanding of risk, enabling insurance providers to offer the most suitable products at the right price. By viewing related quotes even where a key detail such as address or vehicle are different – it is possible to gain a better understanding of the customer where they may have made a change between quotes and at what point they are shopping in relation to the policy start date or renewal date. As well as assisting in risk assessment, shopping behaviour data could support the regulatory reporting requirements by providing known information on customers’ shopping history. Finally, as the FCA rules require renewal pricing strategies to be consistent with current new business pricing, it is more important than ever to use data enrichment for renewal quotes to ensure it aligns with the data enrichment used to price new business quotes. The most sophisticated data enrichment solutions allow risk assessment at individual, asset, household and postcode level with intelligence delivered on all individuals associated with the quote in a single transaction.

Gaining a deeper understanding of the customer will be absolutely critical in this new regulatory environment and that will come from the right blend of insurance specific data, analytics and technology to create an up-to-date and detailed view of the customer both at new business and at renewal.

Source: LexisNexis Risk Solutions

i. https://www.fca.org.uk/publications/policy-statements/ps21-15-general-insurance-pricing-practices-market-study |

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd