By Aman Hanspal, Associate Director, WTW

Except in case of imminent shocks with clear and material transmission channels to the global macroeconomic and political environment. Most geopolitical headlines do not fall in this category of imminent shocks. For investors, it is therefore the longer-term structural and durable shifts, rather than individual events, that matter most in shaping sustained market outcomes. We explore how geopolitical dynamics are evolving, what they may mean for markets and how wealth portfolios can be positioned through periods of heightened uncertainty.

Why is geopolitics becoming more important for investors?

The year has opened with a series of geopolitical events, including renewed US/EU tensions over Greenland, US capture of Venezuela's President Maduro, rising unrest in Iran and subsequent US-Israel military conflict with Iran. Against individual markets, financial markets have generally remained resilient, amidst limited signs of lasting disruption. Even in the case of the ongoing US-Iran conflict, a sustained negative shock to global equities would likely require a significant impairment to key economic channels, which is a plausible outcome but not certain.

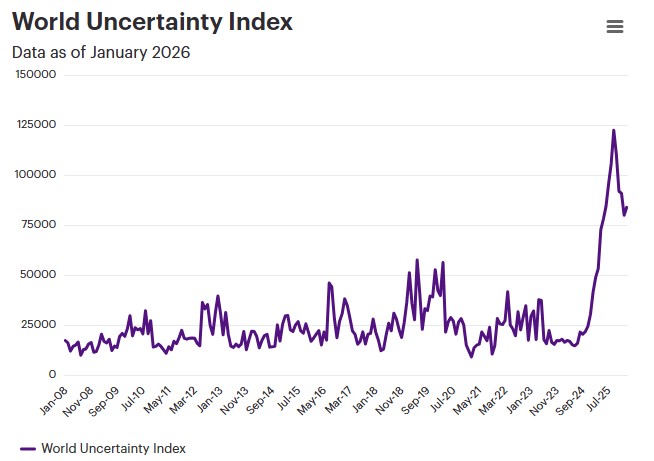

Taken together, however, measures such as the World Uncertainty Index (figure 1), which has risen to its highest level since the global financial crisis, highlight how the cumulative effect of these tensions is creating a more unsettled backdrop for policymakers, businesses and investors alike.

Figure 1: World Uncertainty Index

Behind the scenes, there are signs of a more assertive, resource-focused approach from major powers, particularly the US. Recent actions point to a growing emphasis on securing critical minerals, reshaping trade flows and reinforcing political alliances that support national strategic priorities. This shift, sometimes described as a modern form of mercantilism, represents an important long-term trend. It suggests a world in which uncertainty is structurally higher than it was for much of the post-financial-crisis period, even if individual events matter less.

A more assertive US foreign policy is taking shape

Recent developments appear to form part of a wider strategic pattern rather than a series of isolated incidents. The US is signalling a willingness to deploy a broader set of tools, including economic pressure, trade policy, diplomatic leverage and, where necessary, military force, to protect its interests. These actions point to a strategic environment in which geopolitical influence, economic leverage and resource security are increasingly intertwined. While not every episode will have immediate market consequences, together they contribute to a backdrop of higher strategic tension and greater probabilities of extreme outcomes.

What the US–Iran situation tells us about market risk

The recent escalation involving Iran provides a useful illustration of how markets tend to process geopolitical risk. For markets to be materially affected, disruption usually needs to be sustained and economically meaningful, for example through prolonged shock to global energy commodity supplies or trade routes such as the Strait of Hormuz, through which pass significant portions of global seaborne trade for oil, natural gas, sulphur, fertilisers (used in food production), amongst other commodities used across a wide range of industries. Continued disruption in this area would have the potential to affect global growth and inflation, but even this outcome is not a given.

Importantly, isolated geopolitical events do not need to trigger an immediate market shock to have lasting relevance. Over time, repeated episodes can contribute to slower-moving shifts in policy, behaviour and capital allocation. These behind-the-scenes changes are often where geopolitics has its most lasting influence on markets.

How these longer-term shifts could affect markets

A more inflation-prone environment: Moves towards greater self-sufficiency, re-routing supply chains and higher strategic and defence spending all add to cost pressures. Geopolitical fragmentation tends to reduce the efficiency of global trade, potentially keeping inflation structurally higher than in the decade prior to the pandemicShifts in trade and capital flows: Some US allies in Europe and Asia, which hold large US financial assets, are gradually diversifying their holdings, their relationships and strengthening domestic resilience. Even modest shifts in capital allocation of investors in these economies can influence US and local currencies, government bond yields and relative returns across regions. This has been evident in US dollar weakness and renewed interest in gold amid heightened uncertainty over the past yearDivergence in asset performance: While developed-market equities have remained broadly resilient, outcomes have varied at the sector-level. European defence stocks, industrial metals and parts of the energy sector have benefited from increased security and supply-chain priorities.

These examples underline that geopolitics tends to affect markets less through abrupt shocks and more through gradual changes in policy, incentives and investor behaviour. This environment also creates slowly accruing risks and opportunities, which can be incorporated and managed within well-diversified portfolios through disciplined investment frameworks.

Why perspective matters more than the headlines

With events unfolding rapidly, it is tempting to treat each new headline as a turning point. But geopolitics tends to work on longer timelines. Territorial disputes, shifts in alliances or changes in national strategy usually unfold over months or years, not days. That's why we anchor our thinking in clear trends, focusing on what can be assessed with confidence, where the uncertainty lies and how different scenarios could shape long-term outcomes. By staying disciplined, focusing on fundamentals and keeping sight of the bigger picture, investors can look through short-term volatility and keep portfolios positioned for long-term opportunities while managing the risks of a changing global order.

Disclaimer

Towers Watson Limited (trading as Willis Towers Watson) (Head Office: Watson House, London Road, Reigate, Surrey, RH2 9PQ) is authorised and regulated in the United Kingdom by the Financial Conduct Authority (FCA Register Firm Reference Number 432886, refer to the FCA register for further details) and incorporated in England and Wales with Company Number 05379716.This material is based on information available to WTW at the date of this material or other date indicated and takes no account of developments after that date. In preparing this material we have relied upon data supplied to us or our affiliates by third parties. Whilst reasonable care has been taken to gauge the reliability of this data, we provide no guarantee as to the accuracy or completeness of this data and WTW and its affiliates and their respective directors, officers and employees accept no responsibility and will not be liable for any errors, omissions or misrepresentations by any third party in respect of such data. This material may not be reproduced or distributed to any other party, whether in whole or in part, without WTW's prior written permission, except as may be required by law. In the absence of our express written agreement to the contrary, WTW and its affiliates and their respective directors, officers and employees accept no responsibility and will not be liable. This material is intended for investors with long-term investment time horizons. The value of all investments and the income from them can go down as well as up. This means you could get back less than you invested. Past performance does not predict future returns.

Risk warnings

This document is based on information available to Willis Towers Watson at the date of issue, and takes no account of subsequent developmentsTowers Watson Limited has approved this document for issue to recipients categorised as Professional Clients onlyThis material is intended for investors with long-term investment time horizonsThe value of all investments and the income from them can go down as well as up. This means you could get back less than you investedPast performance does not predict future returnsExpected performance does not predict future returnsTax treatment depends on the individual circumstances of each investor and may be subject to change in the futureThe securities and derivatives investment activities which the Fund engages in may be speculative and involve a substantial risk of lossThe fund may be exposed to credit and/or default risk of issuers of debt securities that may be held within the fundThe issuers of any bonds within the fund may default or not be able to pay the bond income as expectedIf the fund is denominated in a currency other than your home currency, movements in exchange rates may, if not hedged, have a significant impact on the value of (and income from) your investmentShares/units in the fund may become illiquid and investors may redeem their investments only as stated in the fund's prospectus

|