|

|

Inflation erodes the real value of money over time, so investors need to constantly seek out assets that offer returns exceeding inflation to maintain or increase the value of their portfolio in real terms. Chris Pritchard sets out guiding principles for building an investment portfolio that can outperform inflation over the long term. Inflation surged in 2021 as the global economy emerged from the COVID-19 pandemic shutdowns. At the start of 2022, inflation in developed nations reached levels not seen in many years. |

Chris Pritchard, Principal and Co-Head of Insurance Investment at Barnett Waddingham Furthermore, Russia's invasion of Ukraine in February 2022 exacerbated inflationary pressures on the economy. Subsequently, markets have been characterised by persistent inflationary trends, prompting central banks to raise interest rates in an endeavour to rein in inflation whilst trying to steer clear of a recession. This period has been marked by heightened volatility as markets grappled with the repercussions of higher interest rates. Building a portfolio

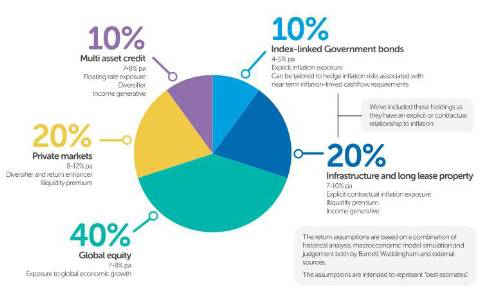

High-level asset allocation Each asset class has been chosen because it has either an explicit or implicit link to inflation, or there are other favourable return characteristics or risk mitigation characteristics. The only two constraints on the portfolio are that no more than 50% is invested in illiquid assets or closed-ended funds and that direct use of leverage is prohibited.

Short-term explicit inflation protection – index-linked government bonds (10%) These instruments provide cashflows directly linked to inflation, offering income in line with inflation to protect against short term spikes in inflation for near-term cashflows (such as employee salaries); Index-linked gilt prices move in tandem with changes in near-term implied inflation, ensuring the portfolio maintains some correlation to short-term inflation expectations; and Bonds historically exhibit low correlation with equity markets over extended periods, providing a natural hedge against a dip in equity markets and enhancing portfolio diversification.

Longer-term contractual inflation – infrastructure and long-lease property (20%) Infrastructure encompasses essential assets vital for a nation's economy, such as roads, airports, hospitals and - increasingly - renewable related assets, requiring significant expertise and upfront capital for management and funding. These assets can be financed through either debt or equity. Long-lease property funds invest in properties leased to tenants under extended rental agreements, typically with inflation-linked rent increases.

Exposure to economic growth – global equity (40%) Inflation and listed equities share a nuanced relationship influenced by various factors. In the short term, rising inflation can impact corporate earnings differently across sectors, with companies possessing strong pricing power potentially benefiting from increased revenues and earnings during inflationary periods. However, sectors like consumer staples tend to be less affected by inflation due to the essential nature of their products and services. Additionally, inflation can influence interest rates and discount rates, affecting borrowing costs for companies and altering equity valuations. Investor expectations about inflation's impact on future earnings can also drive stock prices. Understanding these dynamics is crucial for investors to navigate the complexities of the relationship between inflation and public equities effectively. Both passive and active equity approaches can be taken to diversify and manage risk whilst seeking excess return. Active managers can focus on long-term themes unaffected by economic cycles, offering the potential for added value and outperformance during market turmoil. On the other hand, with its low cost and transparent approach, passive investing provides market exposure based on company market capitalisation. At this time, we would exclude emerging markets due to ongoing high inflation and commodity market disruption.

Diversifiers/return enhancers – private markets (20%) Private unlisted equity provides exposure to economic growth in a similar manner to listed equities. However, there are growth opportunities in private equity markets that are more difficult to come by in listed equities, such as early-stage immature companies with significant growth potential. Private credit provides exposure to nominal growth, but typically with “floating rate” instruments where coupon payments will increase if interest rates increase. This will provide a degree of protection in the event of higher inflation as central banks will likely raise interest rates, boosting the nominal returns of private credit. For clients with climate or sustainability commitments, natural capital assets such as agriculture and forestry are worth consideration. Further detail on this asset class can be found in our recent blog.

Diversifiers in fixed income – multi-asset credit (10%) These funds contribute to portfolio diversification by accessing a broad range of credit assets across the credit spectrum, including investment grade to high yield and direct lending. This diversification can aid in producing attractive risk-adjusted returns with generally lower, though not zero, correlation to equity markets. Similar to private credit, underlying holdings may be floating rate bonds, providing a degree of indirect inflation protection as interest rates rise to combat higher inflation.

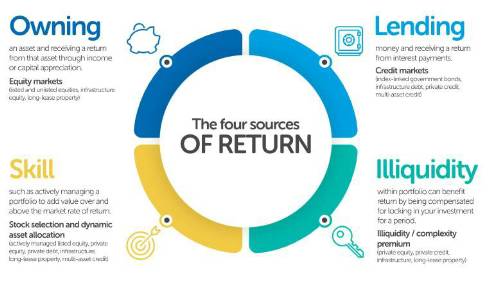

Return drivers

Overall, the breakdown of this asset portfolio should provide investors with: Long-term returns that are expected to exceed long-run inflation; Direct inflation linkage in the short term (primarily useful for those investors with short-term outflows linked to current inflation levels, such as those that needs to pay employee salaries from the assets, which will have a direct short-term inflation linkage); Contractual links to inflation, and implicit links to longer term inflation through exposure to economic growth; Cashflow generation in the short and medium term through credit, infrastructure, and long-lease property holdings; and Diversification across different return sources. This example portfolio aims to provide you with a solid foundation for designing a portfolio that is relevant to your needs. It is important to note that each client will have their own unique set of aims, beliefs, and constraints, which will influence the final composition of their portfolio. Considerations such as returns required, risk appetite, desired level of liquidity, sustinability objectives and governance constraints all need to be considered. |

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd