|

|

UK Consumer Prices Index (CPI) inflation held at 3.8% in September 2025 for a third consecutive month. While the Central Bank expect a steady return to its 2% target over the next couple of years, global tariffs, robust UK wage growth and ongoing geopolitical tensions mean that inflation risk remains. This article explores practical ways that short-term investors can manage inflation risk within their fixed income portfolio through: inflation-linked income (the bedrock of your solution); duration management (keep it low); and active asset allocation and diversification. |

By Hugo Gravell, Principal and Investment Consultant and Chris Pritchard, Principal and Co-Head of Insurance Investment, Barnett Waddingham Protecting against inflation – long-term versus short-term protection

In our article ‘How to build an inflation-beating portfolio’, we set out how investors can build a portfolio to beat inflation over the long term. This portfolio combines assets that are expected to deliver strong inflation-adjusted returns over the long term (like equities) and real assets with a longer-term contractual link to inflation (like infrastructure and property). However, in the short term, these assets don’t track inflation reliably and can introduce other risks – such as illiquidity and price volatility.

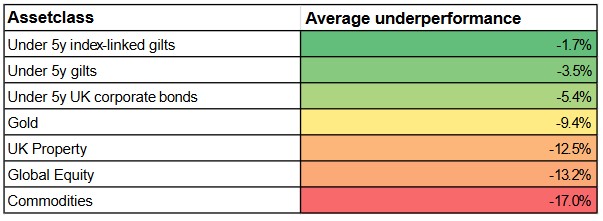

Myth-busting: correlations between asset classes and short-term inflation Over rolling one- and five-year periods since 1986, fixed income assets have outperformed inflation about as frequently as equities and UK property (see Table 1). The critical difference lies in the magnitude of losses when they fail to do so – when equities and property have underperformed inflation, the setbacks are typically far more severe. The same can be said for commodities and gold, which are often regarded as strong inflation hedges. Their short-term performance can be highly volatile and unpredictable, offering no guaranteed protection against rising prices. For example, investors who purchased gold before a downturn in the early 1980s would have waited 25 years before recouping their investment, only to find prices had risen by over 160% over the same period. In our view, the threat of inflation should not distract investors from the role that fixed income can play in their portfolio. Table 1 - Percentage of periods in which asset classes outperformed UK inflation (since 1986 unless otherwise stated)

Source: Office for National Statistics, FTSE International Limited, MSCI, S&P Dow Jones Indices, Markit iBoxx, LSEG Datastream. CPI data prior to 1989 is based on historical modelled estimates of CPI. Based on monthly rolling periods. Table 2 - Average annual underperformance in years when asset class underperforms inflation

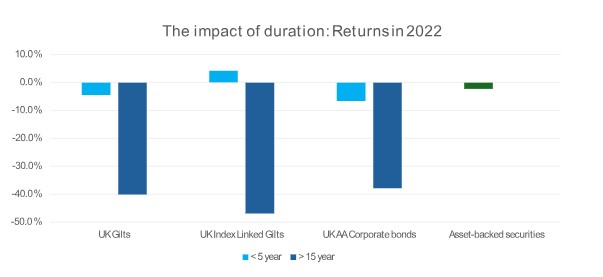

Source: Office for National Statistics, FTSE International Limited, eVestment, S&P Dow Jones Indices, Markit iBoxx, LSEG Datastream. CPI data prior to 1989 is based on historical modelled estimates of CPI. Annual returns on monthly rolling basis. Risks posed by inflation: 1. Purchasing power. Inflation reduces the purchasing power of money. Assets with fixed returns, such as cash and fixed interest bonds, will therefore suffer in real terms. 2. Central bank intervention. Central banks may raise interest rates to combat high inflation, increasing borrowing costs for both companies and consumers. Fixed interest assets are often hit hardest, as investors favour newly issued bonds paying higher interest rates. 3. Supply and demand. Rising input costs and reduced consumer purchasing power can squeeze company profit margins and increase the risk of default for bond issuers with weaker balance sheets. 4. Volatility and uncertainty. Higher inflation can lead to unpredictable changes in asset prices, as investors react to new economic data and forecasts. Assets with a contractual link to inflation Inflation-linked bonds Based on pricing at the end of September 2025, five-year UK index-linked gilts were expected to provide a yield of RPI + 1% (broadly equivalent to CPI + 2%). Inflation swaps Avoiding forced selling Investors will receive the promised yield on bonds if they are held until maturity and do not default, and should therefore aim to hold bonds with maturities aligned to their timeframes. Read about the role maturing bonds can play in our ground-breaking vision for the DC retirement market. Duration management Short-dated bonds: typically with a maturity of under five years, meaning prices are less sensitive to interest rate movements. "High quality asset-backed securities are currently an attractive option for short-term investors. They are backed by a diversified pool of underlying loans, providing a source of regular, stable cashflows, with low sensitivity to movements in interest rates."

Diversification

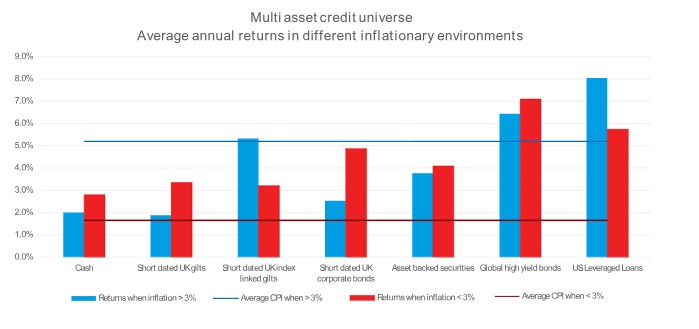

Figure 2 – Annual real returns of fixed income assets in high vs low inflationary periods since 1998. “Short dated” refers to bonds maturing within five years. Conclusions For investors with short-term inflation-linked expenses or strong views that inflation will stay elevated, assets explicitly linked to inflation, such as index-linked gilts, should form the core of the portfolio. Other investors can consider short-term bonds and floating rate assets to generate stable returns while managing the downside risks from persistent inflation, especially when held to maturity. Investors able to accept more risk can consider a multi-asset credit allocation, combining the discussed principles with exposure to higher-yielding assets. |

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd