Richard York-Weaving, Senior Consultant and Katie Garner, Senior Consultant, LCP

Inflation and geopolitics

Since the start of the Iran conflict, the spot rate on one-year inflation swaps has increased by around 1.5% pa, together with upward pressure on longer-term inflation expectations. While the ultimate impact remains uncertain and depends on how the conflict develops, insurers are once again having to consider the risk of inflation re-accelerating.

For now, there is limited evidence of significant inflation emerging within claims experience. Current inflation appears primarily energy-driven, feeding through gradually into other areas. This differs materially from the inflation spike in 2022, where disruption to parts availability and global supply chains increased costs and extended repair times.

Supply chains now appear more resilient. Although shipping routes remain under pressure, supply chains have generally adapted by rerouting around disrupted areas, including via the Cape of Good Hope. The current risk is therefore more linked to sustained cost pressure than supply chain disruption.

For motor insurers, bodily injury inflation remains more nuanced, with wage inflation typically a more significant driver than headline CPI. Wage growth has been cooling into 2026 and, although the conflict may place some upward pressure on earnings, a repeat of the post-pandemic inflation spike in general wages appears less likely given weaker labour market conditions.

For home insurers, inflationary pressures remain closely linked to contractor availability, labour rates and material costs, with sustained energy price increases still likely to place upward pressure on rebuild costs.

Overall, while the current environment does not yet resemble the disruption seen in 2022, it does represent a meaningful increase in inflation uncertainty. For insurers, this may place renewed pressure on pricing adequacy and could shorten the duration of the recent softening cycle.

Pricing

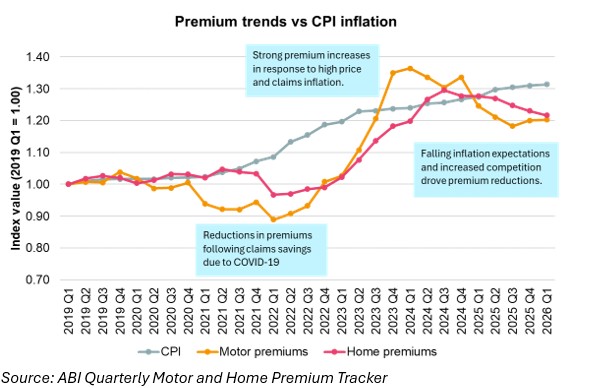

The chart illustrates the path of motor and home insurance premiums since the start of 2019, alongside cumulative CPI inflation over the same period. The market has moved from COVID-driven premium reductions, through a sharp repricing cycle in 2022 and 2023, into renewed competitive pressure more recently.

Although both motor and home premiums are materially higher than in early 2019, the increases have been lower than broader inflation over the same period. Average premiums for both product lines are currently around 20% above 2019 levels, compared with a 32% increase in CPI.

The route to this position has differed between the two markets. Motor insurance saw much larger premium reductions during 2020 and 2021 as insurers reacted to exceptional reductions in claims frequency during COVID-19 lockdowns. It then saw a sharper repricing phase during 2022 and 2023 in response to severe claims inflation. Home insurance experienced a more moderate cycle overall, with less pronounced movements in either direction.

More recently, the market has remained highly competitive, as insurers compete for growth and retention following easing inflationary expectations. There are, however, signs that the motor market may be beginning to turn. ABI data for 2026 Q1 showed average motor premiums increasing by 0.2% following a 1.5% increase in 2025 Q4. While modest in isolation, seasonality matters: Q4 typically sees a premium uplift, whereas Q1 usually experiences a decrease. Against that backdrop, the small increase in Q1 indicates that the softening cycle may have bottomed out.

There is less evidence of a turning point in home insurance pricing. ABI data for 2026 Q1 shows a 1.1% decrease in average buildings and contents premiums.

Historically, motor pricing has reacted more quickly to changing claims conditions and inflationary pressures, reflecting faster claims emergence, shorter pricing feedback loops and the highly price-sensitive nature of the market. Home insurance pricing cycles have generally been more gradual, with insurers typically slower to respond to changing cost trends in either direction.

Frequency trends

If inflation explains why claims cost more, and pricing explains how insurers respond, frequency tells us whether the underlying risk is changing.

For motor, the story is one of relatively contained frequency, with no clear sign of returning to higher claims numbers. Even after a degree of post-pandemic normalisation in driving patterns, the market is not facing a wholesale return to pre-2020 claims frequency. This reflects a combination of factors, including persistent changes in travel behaviour due to hybrid working, ongoing improvements in vehicle and road safety, and lower claims propensity as higher excesses and premium sensitivity discourage claims for smaller losses.

For home, frequency in recent years has been shaped by weather volatility. Subsidence was the standout story of 2025, following the UK’s warmest and sunniest year on record. While wetter conditions in late 2025 and early 2026 may have offered some short-term relief, they do not remove the underlying risk. Subsidence surges no longer appear isolated: 2018, 2022 and 2025 all saw elevated activity. For insurers, subsidence is no longer a one-off aftershock from an exceptionally hot year but, increasingly, a recurring underwriting and pricing issue.

Taken together, the picture is not one of a simple return to the conditions of 2022, nor one of a stable market. Inflation uncertainty has risen again, motor pricing may be approaching a turning point, and weather-driven volatility continues to make frequency unpredictable. For personal lines insurers, the challenge is not just to respond to higher costs, but to recognise how quickly the balance of risks can change.

|