|

|

Pension schemes and annuity portfolios will not escape the effects of Covid-19. At this stage it is unclear how many excess deaths we may see from the coronavirus and that position could change rapidly. If controls on movement prove effective, and the number of excess deaths is around 20,000, then the impact on longevity is likely to be small and mainly down to a reduction in projected mortality improvements. |

By Jon Palin a Partner in Barnett Waddingham’s Longevity Consulting practice. However, we are currently witnessing a rapid increase in deaths from Covid-19 and, if this trend continues, the outlook for pensions and annuities may change significantly in the coming weeks.

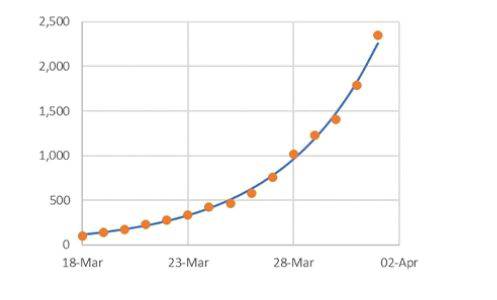

Number of coronavirus deaths

Stephen Powis, medical director of NHS England, indicated on 28 March 2020 that restricting the number of deaths due to Covid-19 in the UK to 20,000 would be a “good result”. The outcome depends largely on the public’s adherence to restriction on movement, with projections of hundreds of thousands of deaths if no action was taken to mitigate the spread of Covid-19. A naïve exponential extrapolation of the figures in the chart above would see over 20,000 Covid-19 deaths by 12 April 2020, so we should have a much better idea of the likely impact of Covid-19 in the next few weeks. (The PHE data is available the next day, and the Office of National Statistics (ONS) data for all deaths registered by 10 April 2020 should be released on 21 April 2020.) However, even if the number of deaths falls in the next month or so, there is still potential for a resurgence in the autumn or winter.

Impact of total Covid-19 deaths on the mortality rate Some deaths that were due to Covid-19 will not have been recorded as such in the PHE data. In particular, it only includes those who were hospitalised. The ONS data records deaths from all causes and provides a separate figure for those with Covid-19 mentioned on the death certificate. Some deaths from Covid-19 may not be ’excess’ deaths, as the deceased may have died from some other cause in the same period, in the absence of the coronavirus. There may be some deaths from other causes that were indirectly caused by Covid-19; for example, if pressure on medical resources caused people to die who would not have died in the absence of the coronavirus. There may be indirect impacts on deaths due to restrictions on movement due to the coronavirus; for example, changes in traffic, pollution and mental health. We need to consider the possible impact on mortality over the following period, rather than just the next few months: The mortality rate could be lower, because coronavirus kills the frailest people, and the remaining population is healthier than average. The mortality rate could be higher, because those who survive the coronavirus are damaged by it – e.g. having reduced lung function. One plausible cause of the low post-2011 mortality improvements is the state of the economy following the 2008 financial crisis, with lower GDP leading to lower tax revenues and lower spending on health and social care. The economic impact of Covid-19 could have a similar negative impact on mortality, depending on the government’s willingness to borrow and spend.

Impact of Covid-19 on socio-economic groups

Impact of Covid-19 on pension and annuity portfolios Higher mortality affects liabilities in three ways:

1. For those who die, the liability is reduced (e.g. a spouse’s pension is payable rather than the member’s pension) or removed.

The UK over-65 population is about 12 million. If we see 20,000 deaths in that age group, then that’s less than 0.2% of the population.

So if deaths were evenly spread among the over-65 population then pension or annuity liabilities could fall by up to 0.2%. In practice the fall could be lower due to spouse’s benefits (not all of the liability being removed) and lower mortality among the more financially material members of the portfolio.

2. Impact on higher base mortality.

If we see 20,000 excess UK deaths in 2020 out of around 600,000 in a typical year, then mortality would be around 3-4% higher in 2020. We would typically do an experience analysis over 3-6 years so an experience analysis might show mortality 1% higher than would otherwise be the case.

That feels small:

in the context of the margin of error in an experience analysis; and in the context of normal annual variations in mortality – e.g. we saw an annual improvement of -3.3% in 2015 due to influenza.

3. Impact on projected mortality improvements.

20,000 excess deaths would likely result in an annual mortality improvement in 2020 of between -3% and -4%.

Section 7.3 of CMI Working Paper 129 shows that a -3% mortality improvement at all ages in 2020 would lead to falls in cohort life expectancy at age 65 of -1.5% for males and -1.1% for females.

However, the impact would strongly depend on the age distribution of the excess deaths in the general population. The Continuous Mortality Investigation (CMI) has indicated that it would consider whether to modify CMI_2020 if Covid-19 leads to an increased number of deaths in 2020 “outside the range of typical annual volatility”. While the CMI has not indicated what the trigger for a change to CMI_2020 would be, we might expect that the scenario with 20,000 excess deaths would be (just about) within typical annual volatility, so not require a change, but (say) 40,000 excess deaths would be likely to lead to a change in CMI_2020. For more information on the measures Barnett Waddingham have put in place to support clients meet the challenges of the coronavirus, visit our Covid-19 response page. |

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd