GlobalData’s Middle East and Africa Reinsurers Database reveals that in 2024, reinsurers in the MEA region posted premiums of $4.4 billion, which represented 1.1% of global reinsurance premiums. Over the period 2020–24, they achieved around a 7.1% compound annual growth rate (CAGR). However, the US-Israel and Iran war is expected to have a major impact on the MEA reinsurers’ operations, as the war’s effect is dual: direct exposure in or near conflict zones raises loss potential and pricing risk, and indirect effects (higher reinsurance costs, global capital movement, inflation) put upward pressure on premiums.

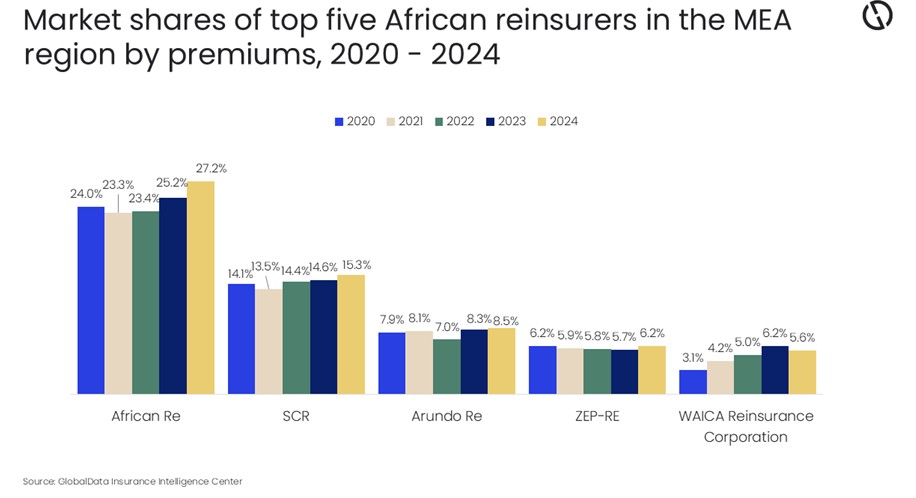

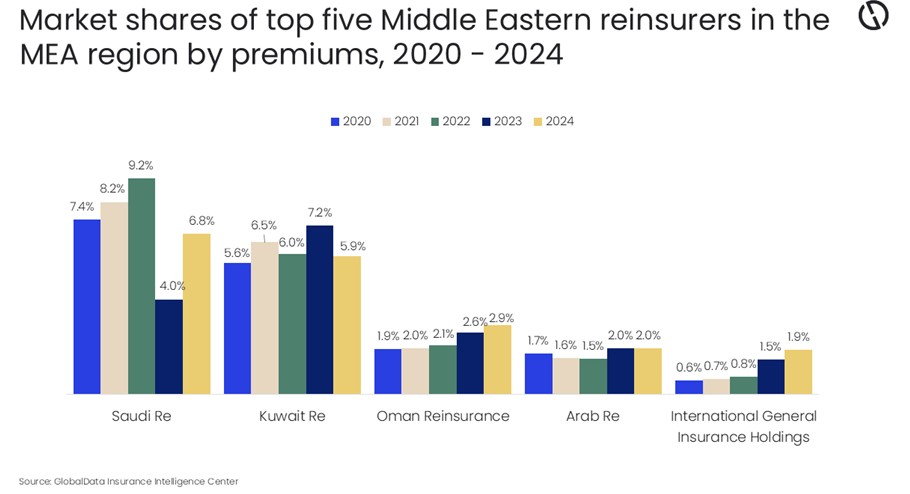

Manogna Vangari, Insurance Analyst at GlobalData, comments: “In 2024, the MEA reinsurance market was heavily concentrated among a few major players, with the top five reinsurers capturing 64.1% of total premiums. African Re solidified its market leadership, increasing its share from 25.2% in 2023 to 27.2% in 2024. Reinsurers based in the Middle East accounted for 20.7% of premiums, with Saudi Re, Kuwait Re, and Oman Re collectively contributing 15.7%.”

While many reinsurers rely largely on international markets for their business, African Re and Arundo Re are exceptions—each earns the majority of its revenue locally in the MEA, at roughly 87.5% and 80%, respectively. By comparison, Saudi Re draws only about 42.5% of its business from the MEA, with the remaining 57.5% from global operations.

Vangari adds: “Reinsurers across the MEA region face mounting pressure. Countries such as Iran, the UAE, Saudi Arabia, Qatar, Bahrain, Oman, Iraq, Kuwait, and Israel are currently grappling with missile and drone strikes, airspace closures, and trade-route disruptions. Specialized insurance lines—marine, aviation, war risk, hull, cargo, and energy—are seeing sharp premium hikes, policy cancellations, and tighter war-risk exclusions amid rising losses.”

Several members of the International Group of P&I Clubs announced that they will cease providing war-risk coverage for vessels operating in and around Iran—including the Strait of Hormuz’ coastal waters up to 12 nautical miles—and throughout the Persian Gulf from March 5, 2026. These decisions reflect heightened security concerns in one of the world’s most important energy corridors.

In the Gulf region, near-term rate increases for the marine hull line are projected at 25-50%, while some underwriters have already cancelled annual hull war policies under standard seven-day war clauses. However, in response to growing war risks and reinsurers’ refusal to cover risks in the region, the US established a major reinsurance facility in March 2026 through the International Development Finance Corporation and the US Treasury Secretary, under which it will provide up to $20 billion in maritime reinsurance (including war risk) in the Gulf region. This is expected to ease reinsurance capacity in the region.

Vangari continues: “Alongside these challenges, reinsurers are investing in AI to enhance underwriting and pricing, and increasingly adopting AI-powered tools to assess risk and improve operational efficiency. Additionally, regulatory shifts in the region are pushing for greater use of technology. For instance, Saudi regulators now require more robustness in operational risk and data management, which strengthens the case for adopting AI and digital tools.”

Innovation is no longer experimental: modular policies, microinsurance, embedded insurance, and parametric triggers are gaining mainstream traction. Collaboration among insurtechs, fintechs, regulatory bodies, and alternative capital providers is accelerating the development and rollout of these offerings. If reinsurers successfully navigate regulatory, data, and operational hurdles, they stand to significantly expand their reach, relevance, and resilience in a rapidly evolving risk landscape.

Vangari concludes: “Reinsurers in the MEA region are generally operating with strong capital buffers. However, they face severe challenges in specialty lines, including marine, aviation, political violence, energy, and trade credit. Their responses so far have been defensive: demanding higher premiums, tightening terms, and reducing capacity. While immediate risks are manageable as long as conflict remains limited in scope and duration, a prolonged or escalated scenario could place serious stress on reinsurance markets and local insurers across the region.”

|