|

|

This update provides the latest estimated funding position, based on adjusting the scheme valuation data supplied to The Pensions Regulator as part of the schemes’ annual scheme returns, on a section 179 (s179) basis, for the defined benefit pension schemes potentially eligible for entry to the Pension Protection Fund (PPF). |

A scheme’s s179 liabilities represent, broadly speaking, the premium that would have to be paid to an insurance company to take on the payment of PPF levels of compensation. This compensation may be lower than full scheme benefits.

Highlights

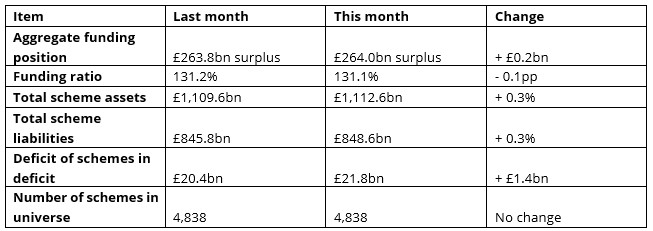

Aaron Pang, PPF Acting Chief Actuary, said: “Market conditions were relatively stable over June. Slightly lower bond yields led to modest increases in liability values, while rising equity markets contributed to a small improvement in the overall surplus position. Against this backdrop, the aggregate funding position of schemes in the PPF 7800 Index remained broadly unchanged. The 4,838 schemes in the index had an estimated surplus of £264.0 billion and a funding ratio of 131.1 per cent. The deficit of schemes in deficit increased by £1.4 billion to £21.8 billion, reflecting the application of PPF drift to some schemes in that group over the month.”

A note on changes to the PPF 7800 Index

In our December 2025 update, we highlighted that the government had announced that it would legislate to allow us to pay prospective indexation starting from 2027 for service accrued pre-1997 for members of schemes who provided this as a right. As well as schemes that have already transferred to the PPF, this will also impact the s179 liabilities of schemes in the PPF universe. In April the Pension Schemes Act received Royal Assent. As we’ve signposted, we’ll reflect the impact from these changes in the PPF 7800 Index in due course.

View the July update and see the supporting data on the 7800 Index for 30 June 2026 here: The PPF 7800 index | Pension Protection Fund.

|

|

|

|

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd