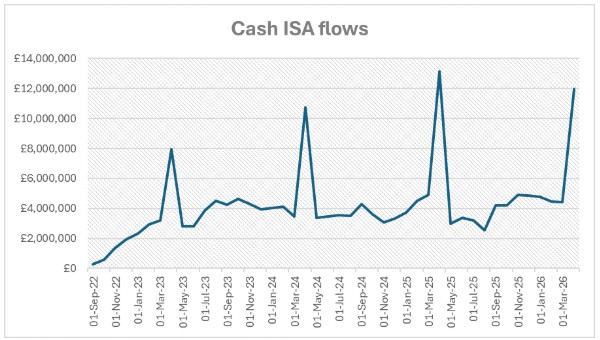

Charlene Young, senior pensions and savings expert at AJ Bell, comments: “A new tax year brings a shiny new set of ISA allowances and savers certainly took advantage, depositing £12 billion into Cash ISAs in April, the second highest monthly inflow on record. While April is always the height of ISA season, this year is the last chance for under 65s to pay in up to £20,000 before their allowance is cut to £12,000 from 6 April 2027.

“Under 65s might be tempted to pile their full £20,000 ISA allowance into the cash version while stocks last, but it’s worth considering if a Stocks and Shares ISA could be a better home for money that you won’t need in the next five years or more. We already had sticky inflation before the Iran conflict, and further surges are expected as the full impact of supply chain disruption and energy shocks filters through.

“While it’s important to have an emergency cash buffer at hand and to keep anything you’re likely to need soon in cash, there’s a significant risk inflation will eat into your interest returns on anything held in cash for the long term. History shows that investing in the stock market beats cash and inflation over the long term, so it could be worth investing money you don’t need to call on for five years or more to give your wealth the best chance to grow.

“There was a surge in money leaving interest-bearing accounts (£13.1 billion), but rather than money being spent and leaving the system, this will largely be explained by the flight into Cash ISAs. There was also a slight increase in money added into accounts that pay no interest, which could be a symptom of the ongoing global uncertainty and worries over cost of living rises to come.”

Source: AJ Bell analysis of Bank of England data. Monthly changes of MFIs’ sterling Cash ISA deposits from households.

Mortgage lending down, but market showing some resilience

“The property market and house prices have started to struggle in the face of falls in consumer confidence, rising unemployment and an energy price cap hike in the offing. Net mortgage lending was down in April to £4.4 billion, from £6.8 billion in March and below the £5.1 billion average over the last six months.

“But there is a glimmer of hope, as April’s approval figures saw another increase to 65,900, above both the 64,000 seen in March and the six-month average of 63,100. This increase in future lending prospects will be down buyers looking to lock in deals as mortgage costs rise. April saw the effective rate on new lending start to creep up, to 4.08% from 4.03% in March.”

|