|

|

Improved funding positions have opened the door for many defined benefit (DB) pension schemes to de-risk their investment strategies and move closer to their endgame. Whether targeting a risk transfer transaction or planning to run on with a low-risk strategy, this shift is prompting the question: is our investment governance model the best fit for our new circumstances? Many schemes use strategic advisers who also help their clients select investment managers on a bespoke basis. |

By Jude Bennett, Partner and Senior Investment Consultant, Barnett Waddingham This model works well for schemes that have the time and resources to be involved in decision making at a relatively granular level. However, there are alternative models if a lighter touch approach is needed.

Two routes to reducing the governance burden on schemes

1. Fiduciary management "Smaller DB schemes may have less ability to tailor the strategy under an FM approach, and so schemes may be paying premium fees for off-the-shelf strategies." This model significantly reduces the governance burden on trustees by outsourcing day-to-day investment decisions. However, FM can be expensive – particularly for smaller schemes – even after accounting for the discounted investment manager fees that fiduciary managers can negotiate in bulk across their client base. Additionally, smaller DB schemes may have less ability to tailor the strategy under an FM approach, and so schemes may be paying premium fees for off-the-shelf strategies. There is also a smaller pool of credible FMs for these schemes to choose from, since many FMs have a minimum investment amount. On top of higher FM fees, best practice encourages trustees to use an independent evaluator to help oversee the fiduciary manager. This introduces further cost and an additional advisor relationship, which may be counterproductive for schemes aiming to simplify governance.

2. Implementation models: a strong alternative "Implementation models can allow tailored strategies to be set up for clients at lower cost than bespoke or fiduciary management approaches." Under an implementation model approach, an adviser may: Streamline the manager selection process by using a panel of high conviction investment funds and strategies likely to meet their client needs. Use a platform or custodian to provide easy access to this panel and simplify the administration of the portfolio. Negotiate bulk fee terms for the panel funds, resulting in cost savings reflective of the total amount invested via the implementation model, rather than on a scheme-by-scheme basis. Continue to provide strategic and manager selection advice but in a more direct way using the panel funds/strategies – this reduces advisory costs while ensuring trustees retain control of key decisions. Implementation models reduce governance demands while maintaining independence from an investment management provider and providing strong cost control. They can allow tailored strategies to be set up for clients at lower cost than bespoke or fiduciary management approaches.

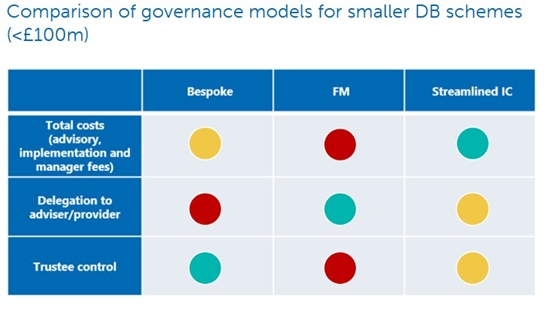

High level comparison: bespoke vs fiduciary vs implementation model These insights are drawn from our practical experience of using these various governance models across a broad range of clients.

The message is that implementation models can fill a gap for clients who want to reduce their governance burden and costs, but who do not want to go down the full delegation route with FM, due to loss of control, cost or other reasons. In our experience with smaller DB schemes, the total costs for a Streamlined IC mandate can be up to half the cost of an equivalent FM portfolio and also typically lower cost than a bespoke approach. Clearly, decisions around investment governance models are not solely determined by cost. However, it is likely to become an increasingly important factor as schemes continue to de-risk and there is less value that can realistically be added through FM or bespoke approaches.

An implementation model in action

A pre-agreed panel of robust, easy-to-understand funds.

Summary However, we think implementation models offer a strong alternative to bespoke approaches or fiduciary management. They combine the strategic independence of advisory models, with some of the improved operational efficiencies of FM – and potentially lower costs than both. Ellie Armstrong, Investment Client Manager, and Henry Redman, Investment Client Specialist, contributed to this article. |

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd