|

|

What to do with a lump sum and how to build a pension back up. Evelyn Partners experts warn: ‘If you didn’t have a plan or purpose for your tax-free lump sum cash, then you need one to protect it from tax and inflation. Even though you can’t just put it back into your pot, it is still possible to build your pension savings back up…’ |

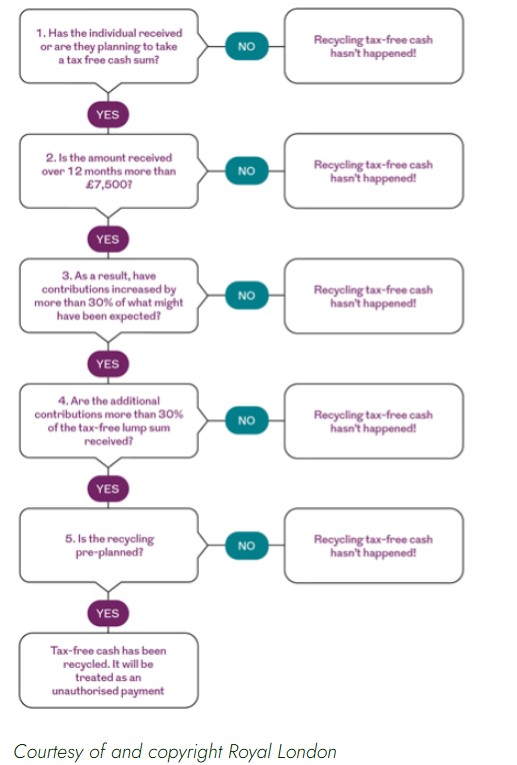

With a 36% surge in pension withdrawals in 2024/25, and much of it coming from tax-free cash, there will be thousands of savers across the UK sitting on lump sums – and many of those will be wondering what to do with it. The ‘pension commencement lump sum’ (PCLS) entitlement to 25 per cent of a pot tax-free (capped at £268,275) has featured prominently in the money pages recently, amid fears the forthcoming Budget could restrict it. Savers are also absorbing the inheritance tax change announced at the 2024 Budget, which means unspent pension assets will become liable to IHT from April 2027. So the pros and cons of taking money out of pensions are being widely debated. Gary Smith, Senior Partner in Financial Planning at wealth management firm Evelyn Partners, asks: ‘So you’ve taken your tax-free cash lump sum – what now? Some savers will have a clear purpose for it, such as paying down the mortgage, home improvements or gifting money to family, and ideally might have done it as part of an advised retirement plan. A bespoke retirement plan might involve saving or investing the tax-free cash to provide a tax-efficient income. ‘But others might be sitting on a lump sum in the bank and wondering what to do with it, especially if they have withdrawn their tax-free cash mainly because of Budget speculation either last year or this year. Taking tax-free cash without a plan can turn a very useful benefit into a bit of a tax headache. Having taken funds out of a tax-protected growth environment, it’s important to protect lump sum cash from tax and inflation. ‘Plus, those who take their PCLS very early in retirement or while they are still working might decide it has left their pot looking a bit threadbare – so can they build their pension back up, and if so how? Might they even build up a new tax-free cash entitlement? Could they fall foul of pension recycling rules? ‘All these are questions that even astute pension savers might not have properly considered – but there are options.’ What to do with a tax-free cash lump sum Smith continues: ‘We always advise our clients to look beyond policy speculation (as recently with the Budget and tax-free cash), remember their long-term financial plan for retirement and not to take any rash steps that they might regret. However, there can be grey areas in financial planning, where it might make sense to bring forward an action that was already planned, and some individuals will just decide to do what they feel is right. ‘Typical planned uses for tax-free cash are to pay down the mortgage or other debts, to gift to family, or to put the funds to work to provide a tax-efficient income through accounts like ISAs. Of course, these options might also be open to someone who has taken their lump sum a bit hastily and is wondering what to do with it.’ Paying down the mortgage Smith says: ‘This sounds straight forward but needs a bit of thought, because someone halfway through a five-year fixed loan for instance might have limited overpayment options. They could have to wait until the deal expires before being able to pay off the lion’s share of the loan, unless they want to pay the early repayment charge. ‘Four years is potentially a long time to hang on to a substantial lump sum, and tax-efficient cash savings options might be limited, so some planning is required. Those who do need to park their cash for a few years will need to keep a close eye on tax exposure (see below), especially as the relatively short timeline might rule out some investment options.’ Gifting Smith says: ‘The patchwork quilt of gifting rules around inheritance tax can be tricky to navigate without advice, so we would always recommend consulting an expert, especially when withdrawing funds from a pension to gift when income tax could be an issue. The annual small gifts allowances can certainly be used but will probably not make much of a dent in a big tax-free lump sum, so really most people will be looking at making large gifts under the seven-year rule, otherwise known as “potentially exempt transfers”. ‘This is something that some savers have decided to do with their lump sum since the 2024 Budget announcement that unspent pension assets will be included in IHT liabilities from April 2027. For instance, with the imposition of VAT on private school fees, we have many clients who are funding their grandchildren’s education from their recently released tax-free cash. ‘The big questions are, can you afford such generosity, in terms of future retirement funding, and are you happy that the funds you’re giving away will be used in a way that you approve of? ‘Making regular gifts using the “normal expenditure from income” rule has become a more widely known strategy – as it swerves the seven-year rule - but those trying to do this without advice need to be very careful as the stipulations are tricky. For instance, what you can’t do is take your tax-free cash, stick it in a bank account and gift it gradually from there, as then it will be seen as a gift from capital and not from income. ‘But one canny option for regular gifting from a lump sum would be to fund the pension of a child or grandchild. While this would probably still be subject to the seven-year rule, it would be tax efficient by accruing tax relief for the pension holder as well as giving their retirement fund a boost.’ Save it or invest it Smith says: ‘A PCLS can form part of a retirement income plan, in which case the adviser will have recommended how to place the funds to give them the best chance of growing tax-efficiently, with the desired level of access and flexibility. But the options might be similar for someone who hasn’t made such a careful plan, as long as the appropriate allowances are available. ‘Unfortunately, what one can’t do is funnel tax-free cash back into one’s own pension - even if it is a different scheme to the one it’s been released from – as that will fall foul of pension recycling rules (see below) and potentially stiff penalties. ‘The big issue with hastily withdrawing tax-free cash is that it’s been taken out of a very favourable tax-free environment, so naturally ISAs will often be the first port of call for idle tax-free cash, and couples can make sure they use both sets of allowances. Likewise, one or both partners might not be using their annual personal savings allowance to the full so then parking some cash in a non-ISA savings account is an option. ‘But with Bank of England rate cuts in the offing, savings rates could be on their way further down, leaving cash savings more vulnerable to inflation. ‘If they have used up ISA allowances, individuals can fund a general investment account, but must be aware that after steep cuts in recent years the annual dividend and capital gains allowances are not generous – at £500 and £3,000 respectively – and it takes careful management to use these exemptions on an annual basis. Offshore bonds can be a capital gains tax-efficient alternative to a GIA for certain clients, but this is very much an area where advice is necessary. ‘Those looking to park a lump sum and who have used up most allowances can also look to cash-adjacent investments like short-duration gilts for potentially better and more tax-efficient returns than deposit accounts. But accessibility might be an issue and constructing a so-called “gilt ladder” - where UK government bonds of staggered maturities can provide a steady income stream – is really a job for the experts. ‘Wealth managers can also offer more sophisticated cash-adjacent portfolios that are designed for parking large cash sums while retaining access and tax-efficiency – such as Evelyn Partners’ “Cash and Cautious Bond” bespoke portfolios. Tax planning and investment management advice can really come into their own once the obvious pension and ISA allowances have been used up, especially where large sums are involved.’ Insure an IHT liability Smith says: ‘For those who are looking at substantial IHT liabilities after pensions are included in estates, taking out whole of life cover can be an efficient way of insuring your inheritance tax liability, so beneficiaries do not have to pay it themselves. ‘You can take out a life insurance policy for all or part of the estimated IHT bill and crucially, have it written into trust so the eventual payout does not form part of your estate for tax purposes. You pay the monthly premiums and when you die the trustees (your beneficiaries) can use the proceeds to promptly settle the IHT bill. ‘These policies can be expensive but if someone has a lump sum they want to use, they could park some of it as a fund to pay premiums that might span many years and really mount up.’ Replenishing your pension pot Andrew King, Pensions Technical Specialist at Evelyn Partners, says: ‘Even careful pension savers might not be aware that as long as they only take their tax-free cash, they can continue to pay into a pension afterwards – in theory, up to the usual annual allowance of £60,000 or their relevant earnings in that tax year. But they do have to try and stay the right side of pension recycling rules (see below) if they have only recently taken their tax-free cash. ‘Many of those taking their PCLS, which is available from age 55 at the moment, will have the means to continue contributing. They could well still be working, or come into an inheritance, or have savings stashed elsewhere that could be mobilised into taking advantage of precious pension tax relief. ‘Even fewer perhaps know that, as long as their tax free cash withdrawal leaves them with some of their lifetime Lump Sum Allowance of £268,275 available, they could also build up a fresh entitlement to tax-free cash (at 25 per cent of their new pot, capped by the remaining LSA). ‘Their remaining legacy pension pot will have gone into a drawdown account, so they won’t be paying into the same pot. They could start a new accumulation account in their workplace scheme or they could start afresh with a SIPP. But they must be careful not to unwittingly restrict how much they can pay in by triggering the money purchase annual allowance.’ Triggering the MPAA Mr King says: ‘How you access your pension is crucial and another reason why those contemplating taking their tax-free cash would be wise to work with an adviser. If you access your pension flexibly or take taxable amounts then you risk triggering the MPAA which will limit future contributions to a maximum of £10,000 a year and could hamper your ability to rebuild your pension pot. ‘When taking the PCLS, as long as you leave the rest invested, or use it to buy a guaranteed income from a lifetime annuity, the MPAA doesn’t come into play. It is however triggered by flexibly accessing a money purchase pension, which typically involves taking an “uncrystallised funds pension lump sum”, starting to draw an income from a flexi-access drawdown plan, buying a flexible annuity, or encashing a pension in full. ‘As the FCA data suggests that at least 54 per cent of those who accessed a pension for the first time in 2024/25 did so in a way that could trigger the MPAA[1], this is obviously not a negligible issue, although it does only limit those who are able and inclined to subsequently pay more than £10,000 a year into their pension.’ Pension recycling King says: ‘Some savers who have withdrawn 25% tax-free cash without a real need for it might think about putting it straight back into their pension – but this isn’t allowed. Even those well informed on pensions can be forgiven for not being totally clear on “pension recycling” rules. These restrictions, established in 2006, are designed to prevent people taking advantage of the pension system by taking money out of pots then putting it back in to benefit from a double helping of tax relief and tax-free cash. ‘The relatively obscure rules have attracted more attention since the last Budget, before which some savers had withdrawn their tax-free cash as a lump sum for fear of restrictions being announced. In the weeks and months following the fiscal statement some pension providers allowed savers to cancel their decision under “cooling off” terms and even allowed others to pay the cash withdrawn back into the pension. ‘Although not technically a pension recycling issue, HMRC and the FCA have this year confirmed that this will not be an option anymore, so savers now tempted to withdraw their pension commencement lump sum – perhaps prompted by concerns over the forthcoming Budget - must now be sure that they have a good purpose and plan for it, as such an action cannot now be reversed without significant tax charges. 'Those who want to build their pot back up after taking their PCLS need to take particular care. This might be the case for someone who has taken their 25 per cent tax-free cash as a lump sum while they continue to work, and wants to ramp up contributions or use a lump sum – an inheritance for instance - to plug the hole in their pension pot.’ The rules have been summarized by Royal London in a graphic which we have included below. King continues: ‘So the key points to watch are the 30% allowance and the timeframe of two years either side of taking tax-free cash. So in other words if you’re paying in more than 30% of the value of your TFC within a couple of years before and after taking that TFC (in other words, a range of five years, including the year in which the TFC was taken), then you might be pulled up and investigated by HM Revenue & Customs. ‘Any increase to contributions is measured on a cumulative basis over the five-year period – a running total of the additional contributions - when trying to determine whether a significant increase has occurred. This could be particularly relevant if the increases in taking tax free cash continue and HMRC view recycling as potentially a more frequent activity. ‘There are no figures on how many savers fall foul of these rules but no one should think they can push the boundaries, as the potential penalties are quite severe, amounting to a charge of up to 55% of the TFC. 'Rebuilding your pot gradually from earnings, bonuses and any other lump sums that become available that is fine, and usually very sensible, but do keep on eye on the recycling rules to avoid any unwelcome attention from HMRC.’ Does taking your PCLS prevent you from using carry forward allowances? King says: ‘Carry forward provisions enable you to mop up any unused annual pension allowances from the three previous years once you have maximised your current tax year’s allowance – as long as you have sufficient relevant earnings in the current tax year. Taking a tax-free cash lump sum does not prevent you from making use of carry forward unless you have triggered the Money Purchase Annual Allowance by taking other funds out as well as the TFC. ‘But if by using carry forward you exceed the limits set out in recycling rules then there is a chance you could be penalised. So for instance, making a very big one-off contribution using carry forward allowances and then taking TFC shortly after could risk a penalty.’

|

|

|

|

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd