|

|

I was in a meeting explaining that we had now implemented the Merz-Wüthrich method to compare against our company’s custom approach for assessing Reserve Risk. I marked this down as a success as the Merz-Wüthrich method is a well established approach, featuring in such places as the Undertaking Specific Parameters in Solvency II. A Swiss colleague interjected, “How can the Merz-Wüthrich method already be considered well established given that the Merz-Wüthrich paper was only published in 2008?” This is a point that is worth remembering - there is currently no established method for measuring Reserve Risk. The problem of measuring Reserve Risk over a 12 month time horizon is relatively new. The pace of the research around the subject has been particularly driven by regulators from the EU and Switzerland. Ten years ago this problem had barely been considered. This article looks at the definition of Reserve Risk and the criteria a good model should meet. It then introduces a practical approach to modelling the Reserve Risk. The key aim in developing this approach was to have a model that is easily applied in practice, yet robust and stable as the business changes over time. The mathematics underlying this practical approach are not as complex as the mathematics underlying the Merz-Wüthrich or Bootstrapping models but thanks to its relative simplicity it offers added flexibility and transparency. The practical approach does not claim to be a perfect measure of Reserve Risk, it claims to be a usable approach that gives an appropriate measure for Reserve Risk. The results of the practical approach are compared to the Merz-Wüthrich because the Merz-Wüthrich method is easy and quick to apply and does not allow for much subjectivity. Nevertheless, like all Reserve Risk models, it is open to challenge, especially given its restrictive assumptions.

Definition of Reserve Risk The risk is around the current reserves - the current reserves have been set using the data available today and using the techniques of today. This is not a measure of the volatility of the past reserving process; it is a prospective measure of the risk around the current reserves over the next 12 months. Many techniques consider the Reserve Risk to be made up of two distinct components; the process risk; and the parameter risk. Simplifying the definitions, they are: • Over the next 12 months the run-off of the reserves is uncertain, even if the link ratios are unchanged from the previous year, the run-off will not be neutral because the incurred claims will differ from expected. This is the process risk. • The link ratios estimated at the end of a period will differ from the link ratios at the start of a period because the additional diagonal will provide additional information. As the link ratios change, so will the estimate of the ultimate. The change driven by link ratios is the parameter risk.

Criteria for a Good Model 2) Adaptable: Reserve data is full of special features, from large claims to changes in claims systems, all of which need appropriate treatment in the modelling of Reserve Risk. Where such features exist the model needs the flexibility to allow for them. In particular the risk measurement should still be able to give good estimates following portfolio changes.

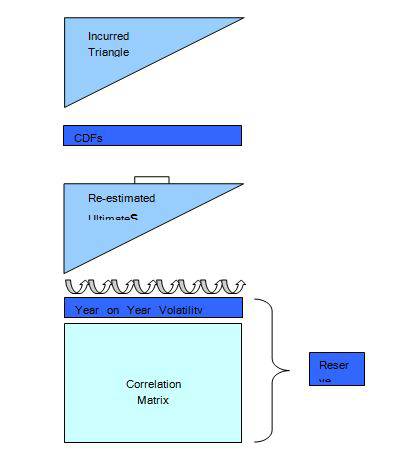

The Practical Approach (based on a Chain Ladder)

The following steps are taken:

Measuring this method against the criteria: The CDFs used to re-estimate the ultimates in this method are the same across all accident years. One interpretation is that such an approach does not capture parameter risk. However, as will be shown later, the risk around changes in the past parameters is captured. In the chain ladder method the main parameter uncertainty relates to the development factors. The estimation of development factors through time may be volatile for two reasons:

i) Estimation Error - The underlying claims development is unstable and the estimation of development factors from historical data contains estimation error. In the absence of other changes, this estimation error will tend to zero as the history used to estimate the development factor increases. The practical approach does not consider these sources of uncertainty separately but allows for them both implicitly.

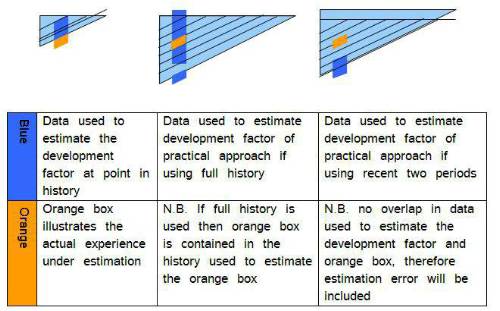

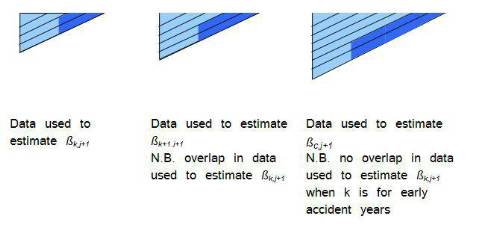

Estimation Error For the past period used to estimate the development factor, no parameter error is measured. When applying the development factor to observations that are outside of this period (i.e. data not used to estimate the parameter), parameter error will be implicitly measured. As long as the full history is not used to estimate the development factor then some parameter error will be included, although it will generally be less than under other methods like the Merz-Wüthrich. This is illustrated in figure 1. Figure 1: Possible data approaches

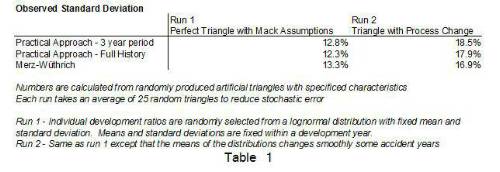

Table 1 shows a numerical example. The practical approach produces lower observed standard deviations than the Merz-Wüthrich. Additionally it can be seen that the practical approach using the full history gives the lowest estimate as this method does not include an allowance for estimation error. However, where the practical approach uses a 3 year past period it can be seen to give a standard deviation 4% higher than that estimated using full history, i.e. the three year period does implicitly include some estimation error.

In some instances, where the full history is used to estimate the development factor, it could be argued that the estimation error is not measured under the practical approach. The actuary would typically choose to use the full history to estimate the development factor for three reasons:

i) The past development has been very stable through time and consequently the full history is a good reflection of the current development. In such a situation the estimation error of the development factor is unlikely to be material as there is a significant and stable history from which the development factor is estimated. In most situations the estimation error will be captured to some degree in the practical approach. Owing to the transparency of this approach, it is easy for a user to assess to what degree estimation error is included. Should the user feel that the estimation error is understated it is a simple matter to alter the calculation to include an additional load. This is something that is seen in practice from the users of this method.

Process Change Under the practical approach, the same development factor is fitted to the entire history. If the development factors have been observed to change over time then the current development factors will give poor estimates of past ultimates. When the past ultimates are poorly estimated then they will appear volatile year on year. If the process change has been more rapid then the development parameters will become out of date more quickly and the measured parameter risk will be greater. Therefore, the practical approach measures the parameter risk in the cases that the development factors have intrinsically changed over time. It is the risk that the parameters are wrong due to process change that is the real risk to reserve inadequacy rather than that they are wrong by statistical chance. We can test how the practical approach compares to the Merz-Wüthrich method in cases where a triangle includes a steady process change. This is shown under Run 2 of the table 1. Run 2 considers a triangle where the development factors change over time - this simulates a process change. Under Run 2 it can be seen that the practical approach measures more risk than the Merz-Wüthrich. This demonstrates that in cases where the parameter has changed in the past due to process changes, the risk of it changing again are implicitly included under the practical approach to a greater degree than under the Merz-Wüthrich. In some circumstances it may be felt to overestimate the parameter risk and again it is easy to understand what could cause this and to make appropriate allowances. In this way the practical approach measures both the process risk and the parameter risk. In some circumstances it may underestimate and in others it may overestimate. The practical approach is understandable and adaptable enough to allow the knowledgeable actuary to make appropriate allowances. See the box ‘Proxy for the Risk’ for a more mathematical breakdown.

2) Adaptable: The re-estimated ultimate triangle can be calculated using many reserving techniques. This allows the flexibility to appropriately measure the risk no matter what characteristics exist in the triangle. There is room to allow for further expert judgement through the use of exclusions or overrides. Where outliers are known and are not expected to repeat in the future, these points can be excluded from the calculation without impairing the method in calculating the risk. Done correctly, it is possible to see instantly what impact this would have on the final result. It is also easy to highlight where exclusions or overrides have been made. This allows for appropriate governance to be built around this expert judgment.

Other advantages

Summary

There are circumstances where any Reserve Risk model becomes less appropriate. It is only by ensuring that the model is simple enough to understand and flexible enough to adapt that these can be adequately compensated for.

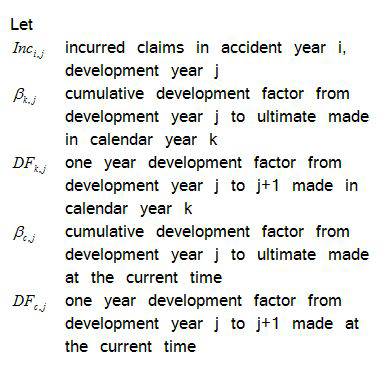

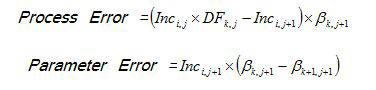

Reserve run-off error in accident year i between development year j and j+1: N.B k= i+j-1

This run off error can be broken down into process and parameter error:

Under the practical approach the reserve run-off error in accident year i between development year j and j+1 is approximated as:

Stable Development

Varying development Additionally, this difference will be amplified as ßc,j+1 is likely to be a poorer estimator for ßk+1,j+1 than ßk,j+1. This is true particularly in older accident years where the data used to estimate ßk+1,j+1 would be distinct from the data used to estimate ßc,j+1 whereas there would be an overlap with the data used to estimate ßk,j+1 and ßk+1,j+1, see illustration. Practical experience shows that the left hand side is larger when development has not been stable over time, i.e. the practical approach would overestimate the parameter risk. Figure 2: Data Used in the estimation of Beta

|

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd

Assessing General Insurance Reserve Risk in Internal Capital Models – A Practical Approach by Henry Medlam, Zurich Financial Services

Assessing General Insurance Reserve Risk in Internal Capital Models – A Practical Approach by Henry Medlam, Zurich Financial Services