|

|

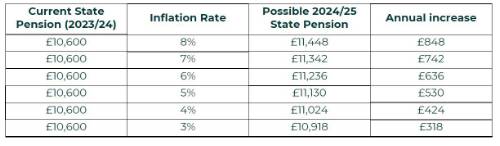

September inflation figure to set triple-lock inflation increase after bumper rise last year. Even if CPI falls to 6% over the next four months, pensioners could be set for £636 annual income boost. |

Pensioners could be set for a major income boost next year as sticky inflation could drive yet another significant rise in the State Pension, says Broadstone. After the government honoured its triple lock pledge with a 10.1% increase to the State Pension for the 2023/24 financial year, those on a full State Pension receive £10,600 a year – an increase of nearly £1,000 compared to the previous year (2022/23). However, inflation is proving more persistent than forecast which could lead to a second consecutive ‘jumbo hike’ in the State Pension. For example, if CPI stays at its current level of 8% the State Pension would rise by £848 to £11,448 a year. Even if inflation drops to 6% it would drive a £636 increase to the benefit.

Damon Hopkins, Head of DC Workplace Savings at Broadstone, said, “Inflation is hammering household budgets, and as we’ve just seen from yesterday’s numbers, there doesn’t seem to be any immediate respite. “While workers may look to their employer for wages to keep pace with inflation, retirees could be set for yet another significant boost to the State Pension. “Having benefitted from around a £1,000 increase to their State Pension last year, another substantial triple-lock hike will further embed its importance to the retirement income of millions of pensioners – present and future.

“Given the delicate state of the government’s finances it will raise further questions around the viability of the triple-lock. That said, it would take a brave Prime Minister to break a key manifesto pledge for the second time in three years so close to a General Election.” |

|

|

|

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

| Contact us about a Capital Contract i... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Head of Insurance Risk | ||

| London - £160,000 Per Annum | ||

| Director - Pensions Risk Transfer (PRT) | ||

| London, Midlands, North West - hybrid working 2dpw in the office - Negotiable | ||

| Dip a toe into public sector work wit... | ||

| Flex / hybrid 2 days p/w office-based - Negotiable | ||

| P&C Consultant | ||

| London / hybrid 3dpw office-based - Negotiable | ||

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd