|

|

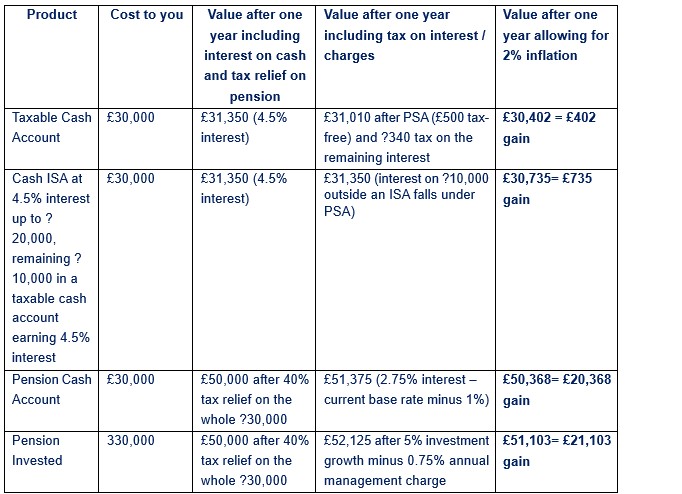

Higher rate taxpayers with £30,000 in a taxable cash account earning 4.5% interest could earn £1,350 a year - but gain just £400 with tax and inflation factored in. Higher rate taxpayers only need just over £11,000 in non-ISA cash savings to trigger a tax bill on their interest. The same £30,000 saved into a pension could deliver a gain of over £21,000 in a year for a higher rate taxpayer, thanks to tax relief and investment growth |

The Bank of England is gradually reducing the base interest rate - but best buy cash savings rates remain around 4.5%, and many households feel they are finally being rewarded for holding cash. However, new analysis from Standard Life, part of Phoenix Group, shows that for higher and additional-rate taxpayers, a significant portion of those gains can disappear once tax and inflation are factored in. While many savers make use of ISAs to shelter interest from tax, those who don’t utilise their ISA allowance – or who have already used the full £20,000 limit – may face a much larger tax bill than expected. With income tax bands now frozen until 2031, more people are moving into higher and additional rate brackets each year, making tax on interest a growing issue for households who may not realise they’re affected. How tax erodes cash savings

Higher-rate taxpayers only need around £11,000 in a non-ISA cash account earning 4.5% interest before their Personal Savings Allowance (PSA)2 is used up and interest begins to be taxed. Even before inflation is considered, this reduces returns significantly.

For a higher-rate taxpayer holding £30,000 in taxable cash:

£1,350 interest is earned at a 4.5% rate

After the PSA and tax, this falls to £1,010

After allowing for 2% inflation, the real gain is just £402

Basic rate taxpayers need around £22,000 to incur a tax bill, and additional rate taxpayers pay tax from the very first % of interest because they have no PSA at all.

The power of pensions

For those able to take a longer-term view, pension contributions remain one of the most tax efficient ways to save. Higher and additional rate taxpayers benefit from enhanced tax relief, giving contributions a substantial immediate boost. Standard Life analysis finds that £30,000 invested into a pension could lead to a gain of £21,103 assuming 5% annual investment growth, 40% tax relief on the whole £30,000 and allowing for 2% inflation - over 52x more than returns on a taxable cash account, and without any immediate tax liability.3 It’s important to note that pensions are usually taxed as income when accessed, beyond the 25% tax-free lump sum.

The potential annual gain of saving £30,000 for a higher rate taxpayer after one year

Inflation calculated on the value after tax on interest and charges for taxable cash account and ISA, and after tax relief, investment growth and charges on the pension. Up to ?20,000 each year can be deposited in an ISA. Mike Ambery, Retirement Savings Director at Standard Life, part of Phoenix Group said: “Higher interest rates can lull people into thinking their cash is working harder than it really is. Frozen income tax thresholds are pushing more people into higher tax brackets each year and the amount of interest lost to tax could come as quite a surprise, especially with inflation to consider too. “While ISAs are a solid tax-efficient option, pensions are where the tax system truly works in your favour. For a higher-rate taxpayer, a qualifying £30,000 contribution can instantly become £50,000 through tax relief. If you’re planning for the long-term, that head start is incredibly difficult for cash savings to compete with.” Mike’s top tips for tax efficient savings 1. Check whether you’re close to breaching your PSA.

“A really important first step is understanding whether you’re likely to breach your Personal Savings Allowance. Lots of higher-rate taxpayers don’t realise that once their cash savings creep above around £11,000, they could start paying tax on their interest. Make sure you know what tax band you’re in, the interest rate on your savings accounts and whether those rates could push you over the threshold.”

2. Make use of your ISA allowance.

“If you’re holding cash that you won’t need immediately, an ISA is one of the simplest ways to stop interest being taxed. Moving money into an ISA is quick, and every penny of growth stays with you. If you’ve used your full £20,000 allowance, consider whether future savings should be directed into next year’s ISA as soon as the new tax year opens. It’s also worth shopping around - ISA rates vary widely and the difference of even half a percentage point can meaningfully affect returns over time.”

3. Think about your savings in buckets

“It can help to divide your money into buckets - cash for emergencies, fixed term ISAs for medium-term goals, and pensions for the long term where tax relief gives your savings a real lift. It’s also worth reviewing these buckets regularly as your life evolves - changes like a new job, growing family, or shifting financial priorities can all affect how much you hold in each and whether your approach is still working for you.”

4. Don’t overlook pension tax relief

“Pension tax relief can make a huge difference, especially for higher and additional rate taxpayers. A good way to think about it, is if you’re a basic rate taxpayer, a £100 contribution will cost £80 as the government tops up 20%. If you’re a higher rate taxpayer, ?100 contribution will cost you £60. “If you’re a higher or additional rate taxpayer, you might need to complete a tax self-assessment to claim higher or additional rate tax relief depending on how your scheme is set up. It’s important to check this with your employer or pension provider.”

5. Focus on the inflation adjusted value of your returns

“Whatever type of saving you’re doing, try to think in terms of what you keep after tax and inflation. Headline interest rates can look appealing, but once tax is deducted and inflation is factored in, the actual value of the return can be much lower. Keeping an eye on the inflation adjusted value of your savings helps you make more informed decisions about where to put your money and ensures your savings are genuinely growing in value over time.”

6. Keep an eye on legislation changes that affect tax and National Insurance

“Frozen thresholds, shifting NI rules, and adjustments to tax allowances can all change how efficient different types of saving are. Reviewing your strategy each year to align with the latest tax landscape can help you make the most of opportunities - whether that’s through pension contributions, ISA allowances, or other tax-efficient savings options.”

|

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd