|

|

In this round of valuations, how Local Government Pension Schemes (LGPS) funds are dealing with climate change will be under the spotlight. We know that funds are at different stages on their journey to managing climate change, but in terms of considering explicitly the impact of climate change on funding, for most funds this will be a first! |

By Melanie Durrant, Partner and Public Sector Consulting Actuary at Barnett Waddingham The requirement to consider climate risk in the valuation followed a recommendation by the Government Actuary's Department (GAD) in their latest Section 13 review of the Scheme, and this requirement has been supported by the Department of Levelling Up, Housing and Communities. Therefore, this is something that all LGPS funds are expected to do, especially given the forthcoming consultation expected to feature climate reporting. But what does that mean for you? We wanted to take the opportunity to summarise BW’s approach to handling climate reporting for the 2022 LGPS valuations.

Our approach

There are four principles which cover the:

scope of the analysis i.e. to identify the impact of climate change on the shorter and longer term funding position in terms of physical and transition risks;

various scenarios to be considered by funds and the impact on their funding position; time horizon over which to consider the risk; and reporting requirements.

In summary, as a minimum, all funds will look at two different climate scenarios and the impact they may have on the funding position over the short, medium, and longer term.

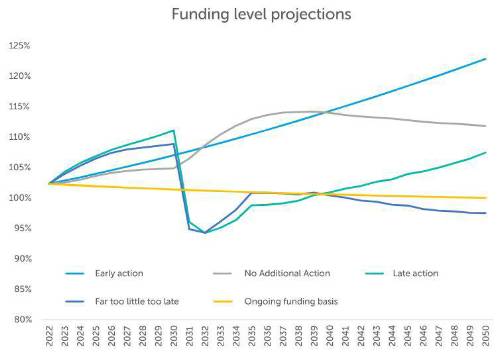

One of the scenarios will be Paris-aligned (seeking to keep the temperature change to well below 2 degrees above pre-industrial levels, ideally 1.5 degrees), assumes good progress towards the Paris ambitions and demonstrates early action in tackling climate risk. This is known as the “Early action” scenario.

The other scenario will be based on higher temperature rises due to late action and/or no new climate policies introduced beyond those already agreed. This will be known as the “No additional action” scenario. “Late action”, which assumes policy implementation is more sudden and disorderly due to delay, resulting in disruption over the medium term. “Far too little too late” accumulates the impacts of the “Late action” scenario and a “No additional action” scenario. The scenario considers what may happen if the implementation of polices is more sudden and disorderly due to delay and, despite action, a larger increase in global temperatures still occurs. Ultimately, our scenario analysis will consider whether the fund’s funding strategy is resilient to climate change, but alongside this, we will recommend other actions that each fund can take in managing climate risk. An example chart can be seen below.

Our analysis will also link climate risk with other risks which we have set out in the table below. The lack of climate data doesn’t make it easy to manage any of these risks specifically in relation to climate risk, but at this stage, it is more about recognising where there are risks and using what information is currently available to manage them.

Employer covenant risk

How might a fund’s employer base be affected by climate change? How is the exposure to the effects of a move to a low carbon economy and what might the effects of physical changes be on them? Are particular employers more vulnerable?

Mortality risk

It’s difficult to say with any certainty how much climate change could affect future life expectancies. This is why it’s more important that ever to do an analysis of your fund’s mortality experience at each valuation.

Legislative risk

We are still awaiting draft regulations in respect of the Task Force on Climate-related Financial Disclosures (TCFD) and how it will apply to the LGPS. However, we are assuming that reporting will be in line with the DWP as some funds are already using the DWP requirements as a guideline.

Other legislative risk comes from governments implementing policies that could significantly increase short-term costs for employers (such as carbon taxes) which could not only affect covenant strength, but also affect investment returns.

Inflation risk

Any climate risk management strategy needs to keep in mind inflation risk, and the part change has in that, as all the LGPS benefits are linked to inflation.

Investment risk

As always, investment risk and funding risk go hand in hand, and any changes to the investment strategy should be reflected in the financial assumptions used to value the fund liabilities.

Some funds have already done this, and already have a net zero pledge in place, so therefore both funding strategy and investment strategy need to be aligned in order to achieve this.

There are lots of actions that funds can take to demonstrate that they are managing their climate risk. Hopefully this blog gives you some insight into the scenario analysis work that we will be providing to funds over the next few months, which has been supported by our specialist sustainable investment team at BW.

We will be engaging closely with our funds on this as we begin to distribute valuation results, but there will be many more discussions to come as we anticipate climate change to be a permanent fixture on the agenda of LGPS funding.

|

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd