|

|

Insurers need more sophisticated credit risk models. We explore this need, considering economic changes, timing, default definitions, diversification, and capital model impacts. Whilst this article has been written with a General Insurance mindset, the considerations noted apply more broadly across Life Insurance and other Financial Services areas. Article 105(6) of the Solvency II Directive discusses the measurement of counterparty default risk - a (re)insurer’s solvency capital is required to reflect potential losses due to unexpected defaults or credit deterioration within the following twelve months. |

By Todd Harrison, Associate and Senior Consulting Actuary from Barnett Waddingham This article also requires consideration of collateral or security held by or for these entities and the associated risks. For most general insurers, the modelling of credit risk is often simple based on materiality and proportionality. However, and albeit with a life insurance focus, the Prudential Regulation Authority (PRA) is encouraging firms to take a more sophisticated approach to their modelling of credit risk, notably around the correlations between different counterparties. This is further backed up by the PRA’s ‘Dear CEO’ letter from January 2024. In this article, we'll highlight why credit risk models should be more complex than current market practice. By examining credit default data, we'll also reveal the key factors you’ll need to consider for better risk assessment.

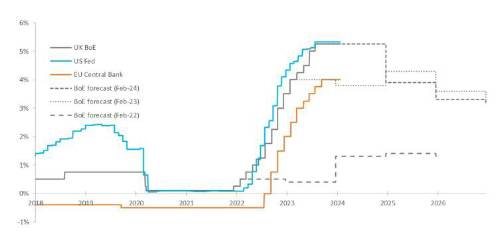

Why now? The time value of money now presents a more substantial risk of mismatch between premium income and claims payments, despite offering greater investment return opportunities. This complexity intensifies with shifts in supply-demand dynamics, geopolitical risks, and the intricate interplay of inverted yield curves.

Historical Interest Rates 2018 - Present

Quite notably, if the Bank of England can get it wrong, then external Economic Scenario Generators (ESG) may themselves also prove flawed, understating the true level of volatility in rates. This was apparent for some of the leading providers last year, and if the experts can get it wrong, then insurers should seriously rethink if their own internal models remain fit-for-purpose.

Interest rates vs credit spreads

2002 dot.com bubble; Periods of economic uncertainty, especially those which are not expected, can lead to adverse changes in the value of an investment portfolio and increase the likelihood of credit defaults. It’s important to understand the risk profile of your underlying asset holdings and their sensitivity to environmental changes, as these factors can lead to unfavourable financial outcomes and impact creditworthiness. Implementing effective credit risk management, along with well communicated processes, controls, and regular reviews of credit ratings enables your firm to respond swiftly to emerging risks that may cause widespread economic distress. "In this regard, a firm’s capital model can and should become a valuable tool for informing the business about potential adverse future scenarios, thereby supporting robust risk management. It is therefore important that we get the modelling right."

Timing matters Over a period of 25 years (1998-2022), analysis of S&P data reveals that twelve out of 25 years exhibited a 0% default rate in investment-grade bonds. Notably, the highest annual default rate of 0.42% was recorded in both 2002, following the dot-com bubble burst, and 2008, amidst the global financial crash. Focusing on the most recent ten-year period showcases a significant upsurge, with 75% of years exhibiting a 0% default rate in investment-grade bonds. Whether this is attributable to volatility, or a changing economic dynamic remains to be proven. What is apparent in the data is that choosing the right time frame when assessing default risk is important, as it can have a significant impact on credit risk capital. Even when considering the leading economic scenario generators (ESGs), it is paramount to consider timing, time horizon and relevance of the chosen indices for the specific use. "Understanding these fluctuations in default rates across varied time periods is useful in developing a robust capital modelling methodology. The capital model should differentiate between an average investment year, the current market climate, and periods of market stress, where default probabilities might notably surge." Given the (relatively) low level of default for investment-grade bonds, it should be noted that the risk of a downgrade is principally what impacts a firm’s portfolio value rather than the risk of an outright default. Whether to contemplate similarly for government bonds is an interesting thought, albeit beyond the scope of this article.

Is the traditional definition of a default still relevant? "From a solvency perspective, capturing the company's bottom line is what matters in the capital model. Missed bond payments might occasionally lead to liquidity issues or, conversely, merely pose administrative inconveniences. It is therefore important to strike a balance between prudence and real-world applicability within the capital model when thinking about default triggers."

Diversification as a mitigant Conversely, it is worth noting that there is a limit to how much credit default risk can be diversified. Some elements of default experience will be correlated across bonds, so even if you were to hold an enormous number of bonds, the portfolio default experience will inevitably still vary over time. What it means for capital models

This solvency article raises some interesting capital modelling design questions:

Regardless of your design choices, it is important that the business ensure that controls and feedback loops are in place to appropriately understand, monitor and communicate changes in the landscape as they may arise.

It can be tough to justify when a complex natural catastrophe has not been fully captured by the capital model, so it might be even more difficult to justify if the model has not fully captured a simple credit default on bonds. "In this sense, what-if and counterfactual analysis can provide useful tools to understand the risks underpinning your investment portfolio and inform the complexity of the modelling approach and potential value at risk from bond defaults." |

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd