|

|

With pressure growing on the UK’s public finances, the government is focusing more closely on the cost of the State Pension. Jack Carmichael and James Jones-Tinsley examine one of the key issues that may come under consideration: whether to introduce means testing. The State Pension system is now under review as part of the recently announced revival of the Pensions Commission. With demographic and fiscal pressures continuing to build, this is likely to prompt reform and renewed debate about issues such as means testing, retirement fairness and how longevity risk is shared across society. |

By Jack Carmichael, Associate and Senior Consulting and Longevity Actuary and James Jones-Tinsley, Self-Invested Pensions Technical Specialist, Barnett Waddingham While not specifically mentioned in the 2025 Pensions Commission announcements, means testing of the State Pension is likely to be one of the areas the Commission considers. Reasons for introducing means testing: building a “fairer” system Longevity risk is a topic I always find interesting, and the State Pension is arguably one of the largest fixed-income retirement arrangements in the world. 1. Redistributing retirement income to those who need it most

The State Pension provides a fixed income of up to £12,548 gross a year. That means public money is also paid to higher earners, some of which could instead be directed towards improving retirement outcomes for lower earners. Higher earners also tend to live longer than lower earners, meaning they are likely to receive more State Pension over the course of their retirement.

Analysis from the Institute for Fiscal Studies shows that, for the lowest fifth of pensioners, the State Pension makes up around 70% of total retirement income. These pensioners are therefore only slightly above Pensions UK’s minimum retirement standard of £13,400 a year. Many are likely to fall below that level if they rely solely on the State Pension. By contrast, for the top fifth of earners, the State Pension accounts for around 20% of total retirement income. Redistributing State Pension support from the highest to the lowest earners could therefore improve retirement outcomes for millions of lower-income pensioners. 2. Providing an additional lever to protect against State Pension Age rises

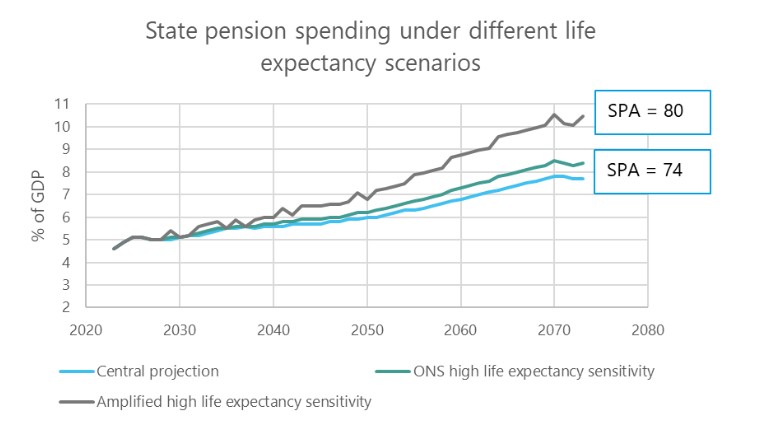

At present, the government has limited options for managing the cost of the State Pension, with the main lever being the State Pension age. The cost of the State Pension is expected to rise as the UK population ages, and analysis from the Institute for Fiscal Studies suggests that the State Pension Age may need to increase to 74 to balance the total cost.

My own analysis suggests that, if life expectancy rises by more than expected, the State Pension Age could, in an extreme scenario, need to increase to 80.

Means testing would therefore give the government another lever to help manage the cost of the State Pension. 3. State Pension as a form of longevity risk insurance

As demographic pressures build on the UK retirement system, is it time for a more radical rethink of the State Pension?

One possibility is to view it as a form of longevity risk insurance, rather than as a uniform level of income. The state is well placed to help manage longevity risk across the population. It could help pensioners manage the long-term risk of running out of money if they live longer than expected. The system could include means-tested, age-based increases that activate for older pensioners. Such a system might help encourage individuals to save more for retirement. It could also create greater scope for retirement products that pay more at younger ages, when pensioners are in the spending phase of retirement. Reasons against introducing means testing Jack raises some interesting points, particularly from an actuarial perspective on the State Pension system as a whole. I want to look at some of the reasons why means testing may not be the right approach, drawing on my background in individual retirement planning and focusing on how it could affect retirement outcomes. 1. Undermining incentives to save for retirement

One of the biggest risks is that means testing could discourage people from saving for retirement if higher savings reduce their State Pension entitlement. This may be particularly relevant for lower earners, who may be more likely to reduce their pension contributions.

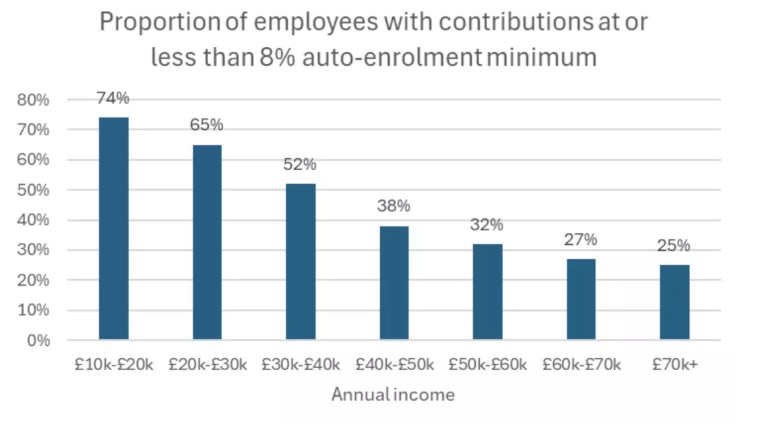

The UK is already facing a significant retirement savings challenge, with many people either under-saving or not saving at all. Analysis from the Department for Work and Pensions suggests that: Only 25% of individuals earning less than £10,000 per year are saving into a pension.75% of individuals earning between £10,000 and £20,000 a year are, at most, saving at the minimum auto-enrolment contributions level of 8% of salary.

Retaining a uniform State Pension reduces the risk of lower-income savers being discouraged from saving into a pension. 2. Other areas of focus, such as the State Pension triple lock

There is a range of public analysis highlighting the cost of the triple lock, which, as Jack notes, may disproportionately benefit higher earners who tend to live longer. These include:

Analysis from the Institute for Fiscal Studies suggesting that, since 2011, the triple lock has added £11bn a year to the cost of the State Pension.Analysis from the Office for Budget Responsibility suggesting that the triple lock could add £43bn a year to the cost of the State Pension in the early 2070s. These are significant costs for taxpayers. A fair question is whether some of that spending could instead be used to increase the base level of State Pension income. Several suggestions have been made about how the triple lock could change. However, any reform would be politically controversial, and the main political parties have tended to treat the triple lock as close to untouchable. 3. Administrative complexity and costs

One obvious disadvantage of means testing is the additional administrative complexity and cost. There are several international examples of means-testing systems operating successfully. One example is Australia, which uses a combination of income- and asset-based means testing. However, analysis of UK and international means-tested schemes suggests that introducing a means-testing element could increase the administration costs of the State Pension by a factor of three to four.

There is also a risk that added complexity could discourage people from claiming other means-tested benefits. In the UK, it is estimated that around 38% of eligible pensioners do not claim Pension Credit, possibly because of the complexity involved in claiming it. 4. Public reaction

Discussion in the press about changes to the State Pension, whether financial or age-related, is often met with strong public criticism. Comments responding to Jack’s recent press coverage highlighted a widely held view that the State Pension is an entitlement earned through a lifetime of National Insurance contributions, rather than a benefit in the same sense as other forms of state support.

Public and political opposition to something as fundamental as means testing would be substantial. It would take a very bold politician to propose a policy that may deliver no savings for five to ten years, yet prove immediately unpopular with the electorate. So, should the State Pension be means tested? As Jack and James have highlighted, any move towards means testing would have implications well beyond the State Pension itself, touching everything from retirement saving behaviour to perceptions of entitlement and fairness in society. Trade-offs are unavoidable, and the 'right' answer depends on priorities as much as economics. The complexity of the issue, combined with the public sensitivity around pensions, makes this one of the most politically difficult debates in UK retirement policy. |

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd