|

|

Given the delayed release of CMI_2022 (the most recent version of the mortality projections model produced by the Continuous Mortality Investigation), it can be easy to forget that the next model is only three months away. However, CMI_2023 will be here before we know it (est. March 2024), bringing with it another year of data and more complex calibration decisions. |

By Hande Love. Senior Consultant, Nicola Torley, Consultant and Kara Scott, Associate Consultant from Hymans Robertson In this article, we consider what the 2023 mortality data looks like so far, and what the impact of incorporating new data into the CMI model could be. We also highlight some key considerations for users of the model, including the potential materiality of weight parameters (which enable users to flex the allowance made for individual years of data). What this brings to light is that blindly using the old, mostly data-driven, approach to setting assumptions no longer works, and focussing on the bigger picture will be crucial.

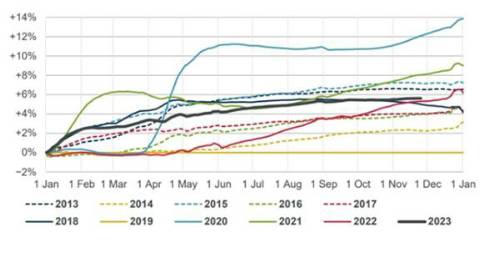

2023 mortality so far The chart below provides this picture for 2013-2023, showing how the cumulative mortality rates in England and Wales (E&W) each year compared with those in 2019. Focusing on 2023 (the bold black line), the cumulative mortality rate to week 47 was 5.6% above that in 2019, but close to the equivalent period in 2022. Cumulative standardised mortality rates for England & Wales compared with 2019.

Chart source: CMI mortality monitor – week 47 of 2023 (© Continuous Mortality Investigation Limited). Use of this CMI information is subject to the CMI’s Disclaimer notice included at the end of this article. This is not the positive, post-pandemic picture we wished to see. To make things worse, almost half the excess deaths observed in 2022 occurred in the last three months of the year, so there is still time for 2023 experience to ramp up further. Only time will tell. Those with more optimistic mindsets might remain hopeful that the end-of-year comparator remains below +6%, particularly with the excess mortality rate levelling off in recent months.

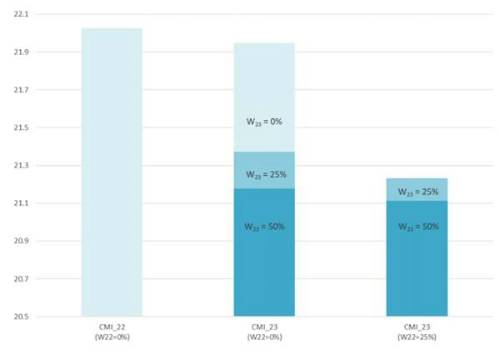

Analysing a ‘proxy’ CMI_2023 model Even if the future core weights were known for certain, it remains important for companies to carry out their own analysis to determine a suitable model calibration. Relying on core weights may be the ‘easy approach’, but it risks herding in the market and can lack rationale (ultimately making it more difficult to justify the approach to stakeholders). Further, and most importantly, there is no guarantee that they will produce improvements that reflect the ‘real-world’. For CMI_2023, users will not only need to choose what weight to place on 2023 data, but also to consider the interaction between the 2022 and 2023 weights. This will involve a lot of thinking, but users can get a head-start by using a ‘proxy’ CMI_2023 model to derive initial estimates. And we have done exactly this. Using a combination of estimated 2023 deaths[1] and exposures[2], and the existing CMI_2022 model, we assessed the impact on life expectancy of a sample of ‘CMI_2023’ weight combinations. The results were calculated using the CMI’s core parameter values (except the weightings) and a long-term rate of 1.5% per year and can be seen in the chart below. Comparison of cohort life expectancies for men aged 65 in 2024, under different CMI models and weight parameters (W).

Note: Use of the CMI model (© Continuous Mortality Investigation Limited) is subject to the CMI’s Disclaimer notice, which can be found in the ‘Notices’ tab of the model. Of course, we will need to wait and see where the 2023 experience ends up but, using our ‘proxy’ model, we see that the choice of 2023 weight could be a material decision for users of the model. For example, applying 0% weight to 2022 data and varying the 2023 weight between 0% and 50% (middle column on the chart) produces life expectancies for a 65-year-old male in 2024 ranging from 21.9 years to 21.2 years. This is a difference of 3.5%, which could have a comparable impact on liability values. The chart also shows the potential result if the CMI stick to their original plan of increasing the core weight for each upcoming year of data by 25 percentage points. In that instance, applying 25% weight to 2022 data and 50% weight to 2023 data (dark blue stack in the right-hand side column) produces a life expectancy of 21.1 years for a 65-year-old male in 2024. This is a really low value. To put it into context it’s lower than placing 100% weight on 2022 data, which in itself would have been considered quite a bold choice. There is therefore an onus on the user to make their own choice about an appropriate parameterisation.

Other considerations for the CMI model Different weight combinations can produce equivalent results. For example, applying 0% weight to 2022 data and 50% weight to 2023 data (dark blue stack in the middle column above) produces a similar result as applying 25% weight to both years of data (combining the dark blue and mid-blue stacks in the right-hand side column). This prompts the question – if multiple combinations produce similar results, how can one calibration be justified over another? It will be interesting to see if companies maintain existing weight choices and simply update the new weight each year, or whether they adapt all weights to achieve an appropriate result. Although the weight parameters are independent levers in the model, their impact depends on the choice of other parameters. As such, users need to consider the interaction between all parameters (Eg the smoothing parameter, the initial addition to improvements parameter etc.) to ensure that the overall result reflects the intended population. These interactions can also add complexity when comparing different sets of results, where individual parameters are often compared. With more and more parameters added to the model each year, comparing individual parameters may become less valuable, whilst a focus on the bigger picture could be more useful. For our longevity benchmarking survey report this year, we used the calibrations submitted by participants to calculate the associated initial improvement rates. This enabled us to provide that overall view and a more holistic comparison than just the individual parameter differences. Our benchmarking survey this year also highlighted that many insurers and reinsurers who are placing 0% weight on 2022 data are allowing for excess mortality in other ways. Although not many companies were using the new mortality overlays feature in the CMI_2022 model for this, it will be interesting to see if the usage increases in future years, eg as the functionality is better understood, or if the use of overlays in general increases. Either way, no matter how they are allowed for, these alternative adjustments will need to be revisited to consider allowance for 2023 experience. Finally, CMI_2023 is expected to include updated population estimates for 2012-2020, following the 2021 census. These updates will likely impact the overall level of improvements implied by the CMI model, so users will have to consider whether the new population estimates affect their overall view. We can see that setting a trend assumption using the CMI model isn’t getting any easier, and the default projection now involves a lot more judgement than it has in the past. This means users must make use of additional sources of information beyond the recent population mortality data to set a sensible assumption.

[2] We estimated the population values using an equivalent approach as the CMI used for 2022. |

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd